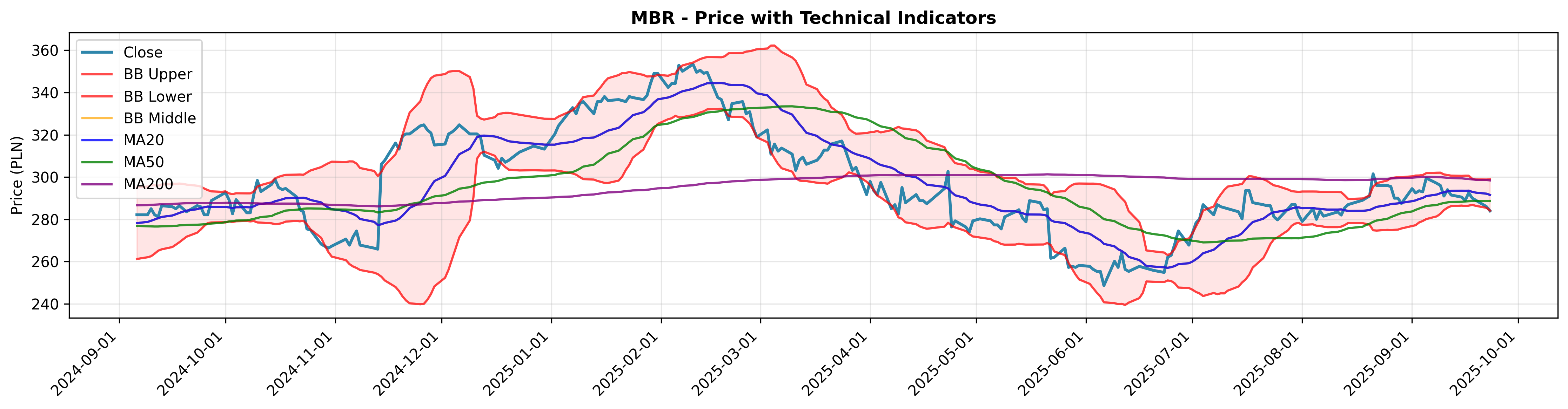

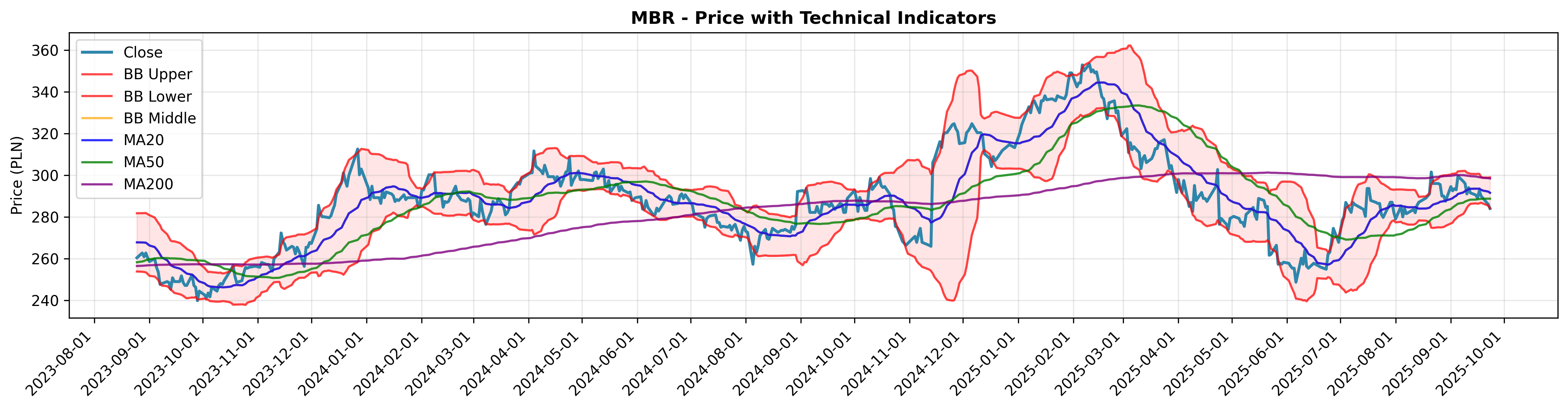

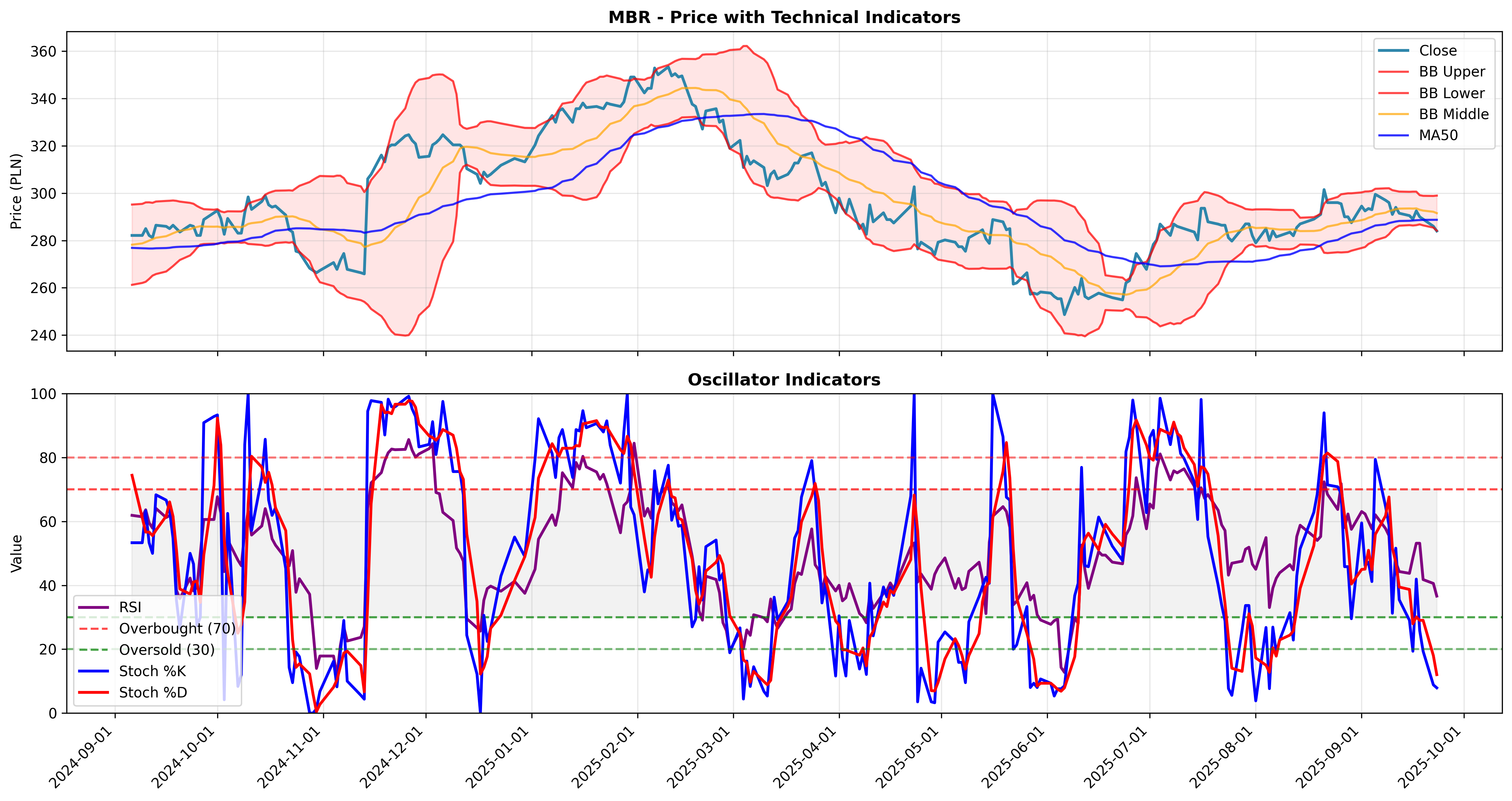

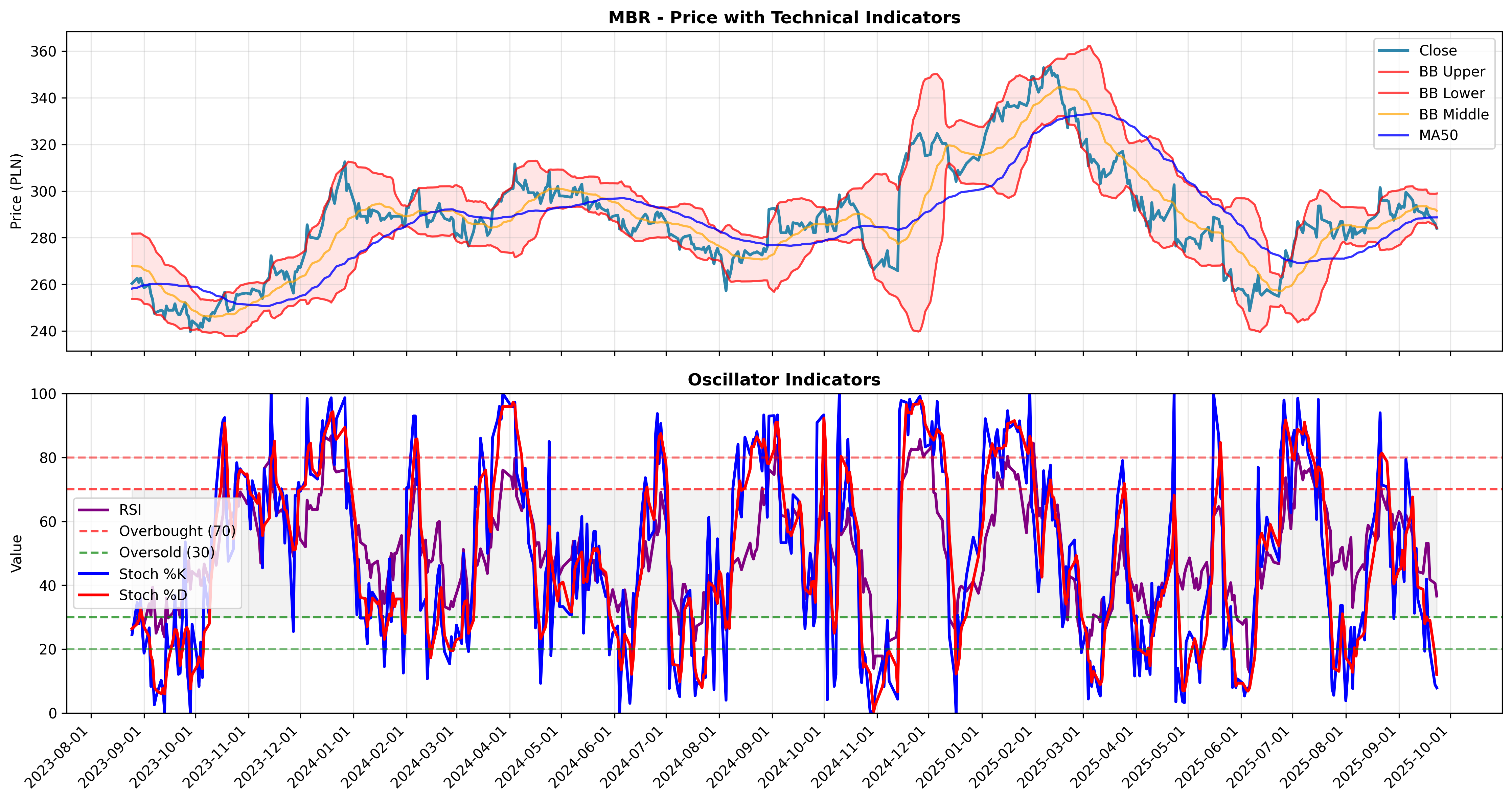

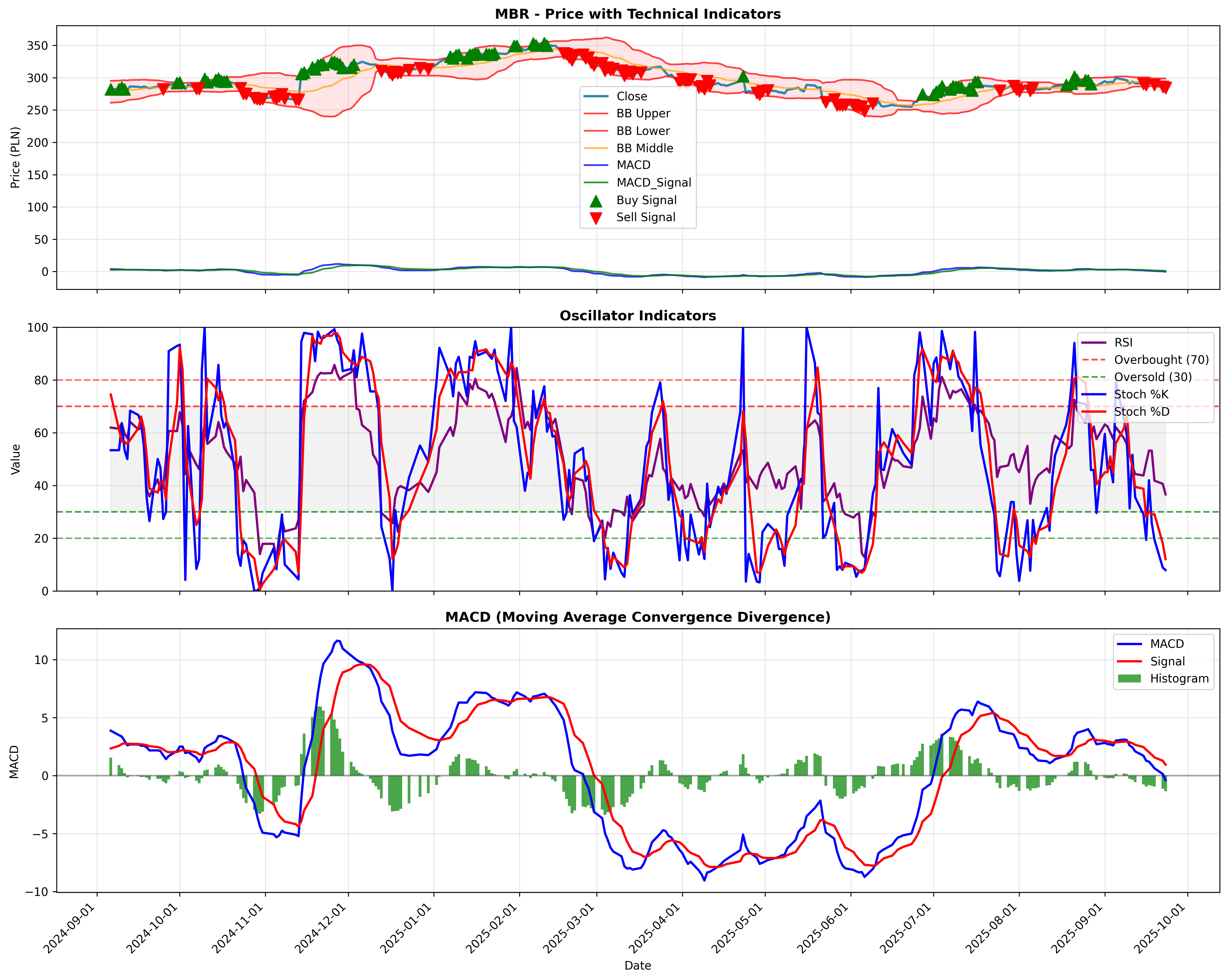

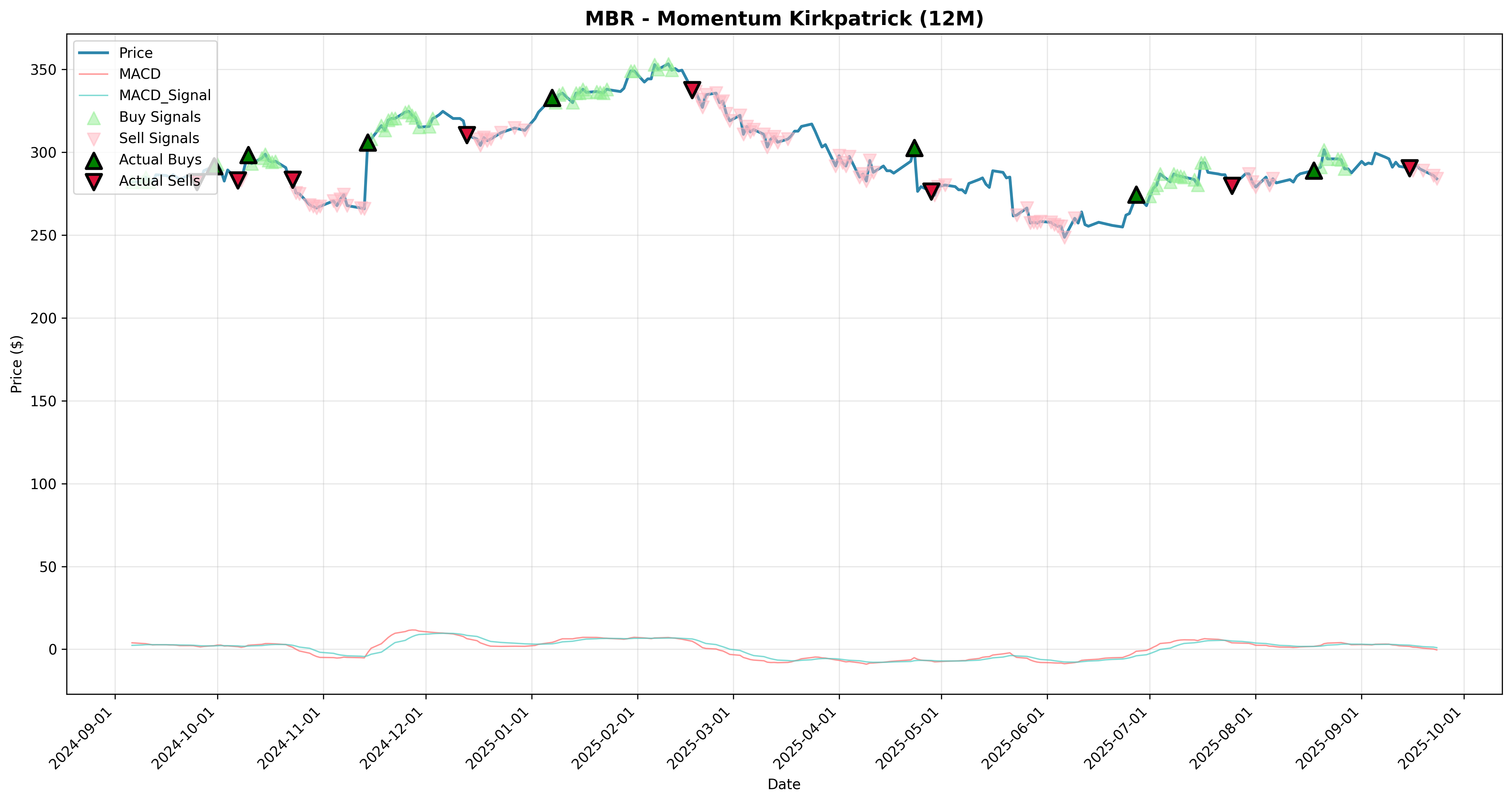

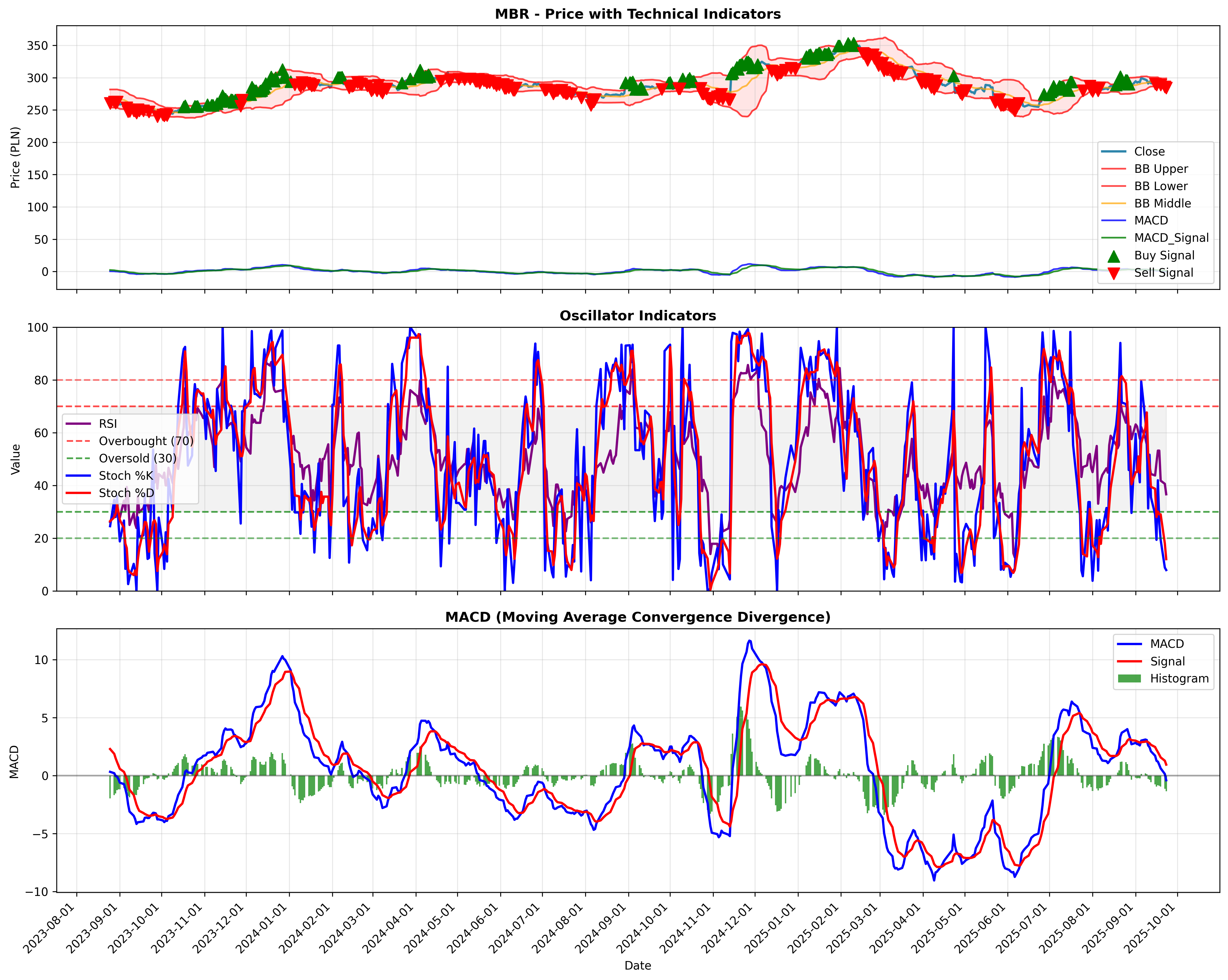

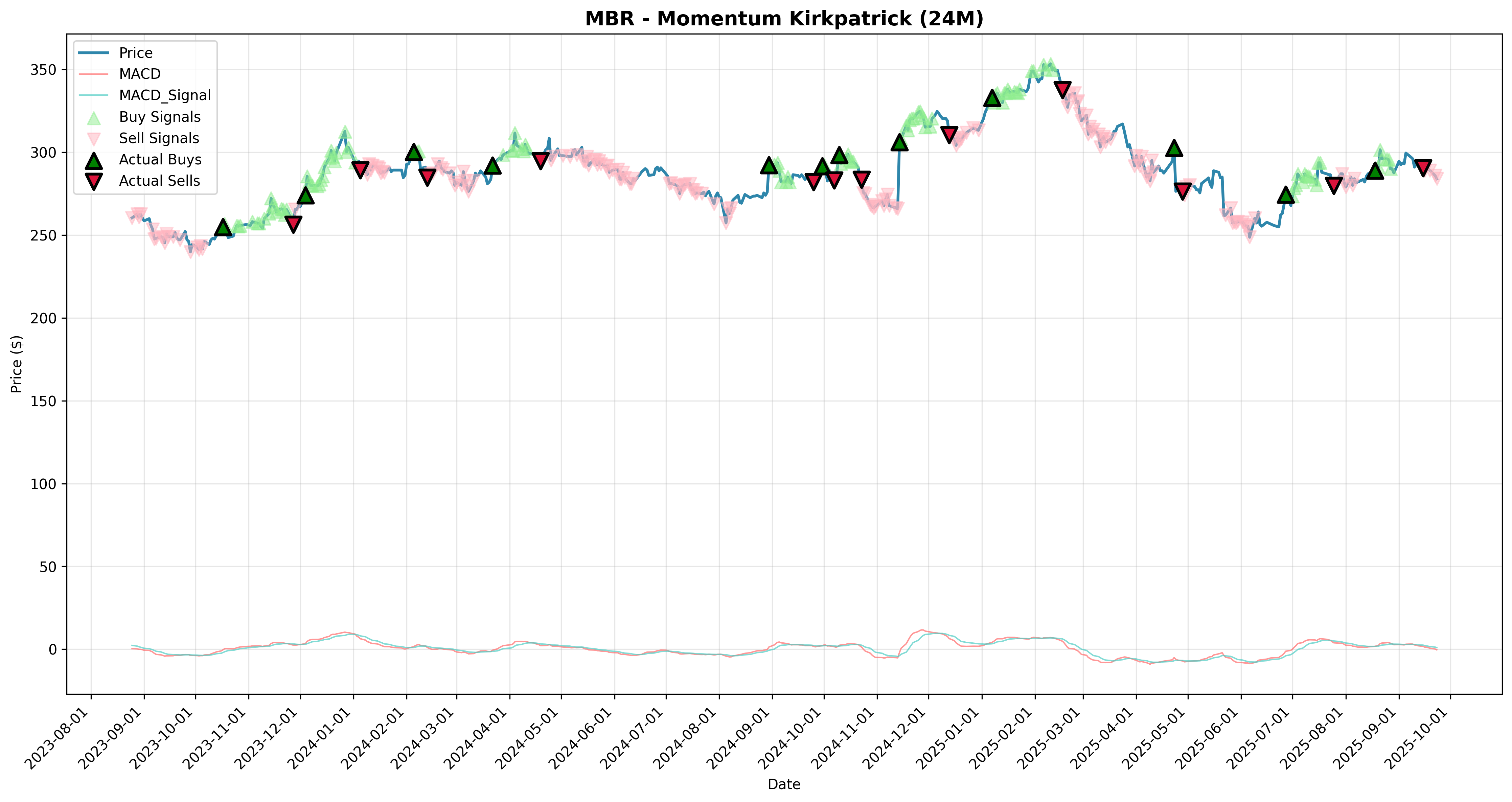

MBR Stock Analysis

Summary

Backtest Summary - MBR

Generated: 2025-09-24 06:29:06

📊 Buy & Hold Benchmark

Total Return: +398.85%

Analysis Period: Medium-term

Date Range: {‘start’: Timestamp(‘2010-06-29 00:00:00’), ’end’: Timestamp(‘2025-09-23 00:00:00’), ‘days’: 5565}

This represents the return from buying at the start and holding until the end of the analysis period.

Performance Overview

| Strategy | Symbol | Total Return | 3M Return | 6M Return | 12M Return | 24M Return | Excess Return | Sharpe Ratio | Max Drawdown | Trades | Win Rate | Final Value |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| trend_momentum | MBR | 461.83% | 1.3% | 1.3% | 11.0% | 22.8% | 62.98% | 0.40 | -70.49% | 41 | 48.78% | $561,830 |

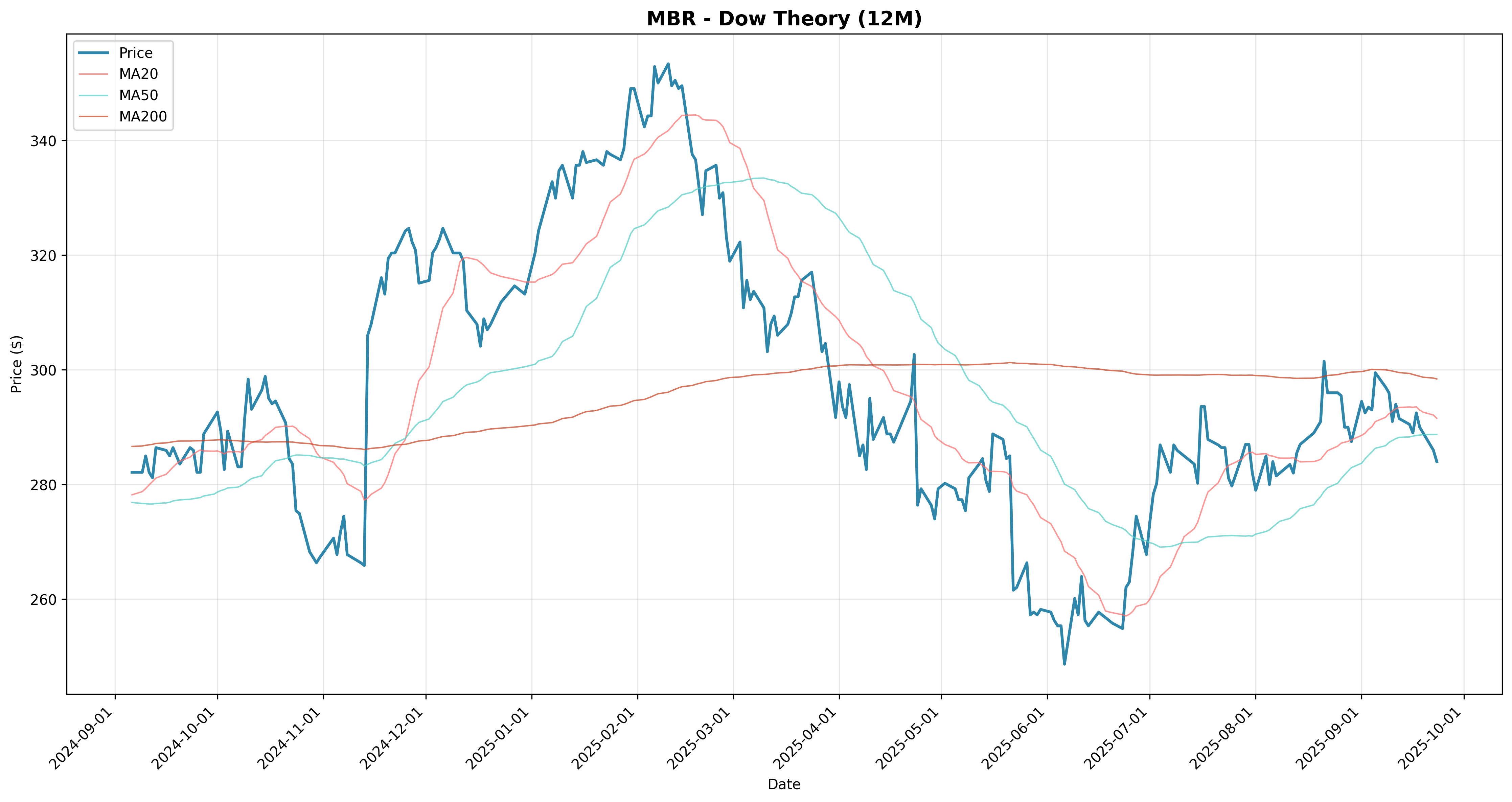

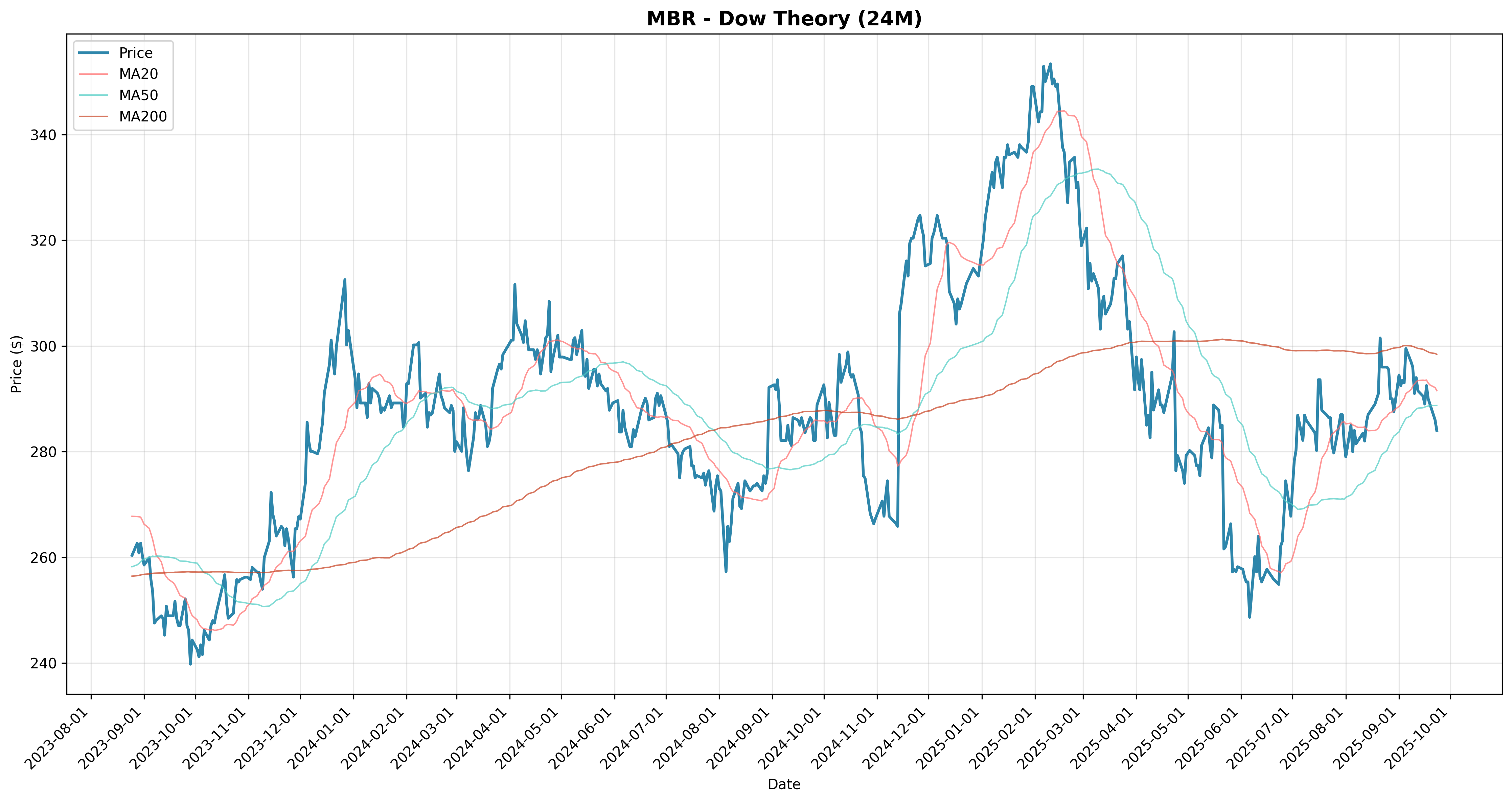

| dow_theory | MBR | 2857.30% | 11.4% | -10.4% | -0.9% | 12.6% | 2458.46% | 0.00 | 0.00% | 1 | 0.00% | $2,957,301 |

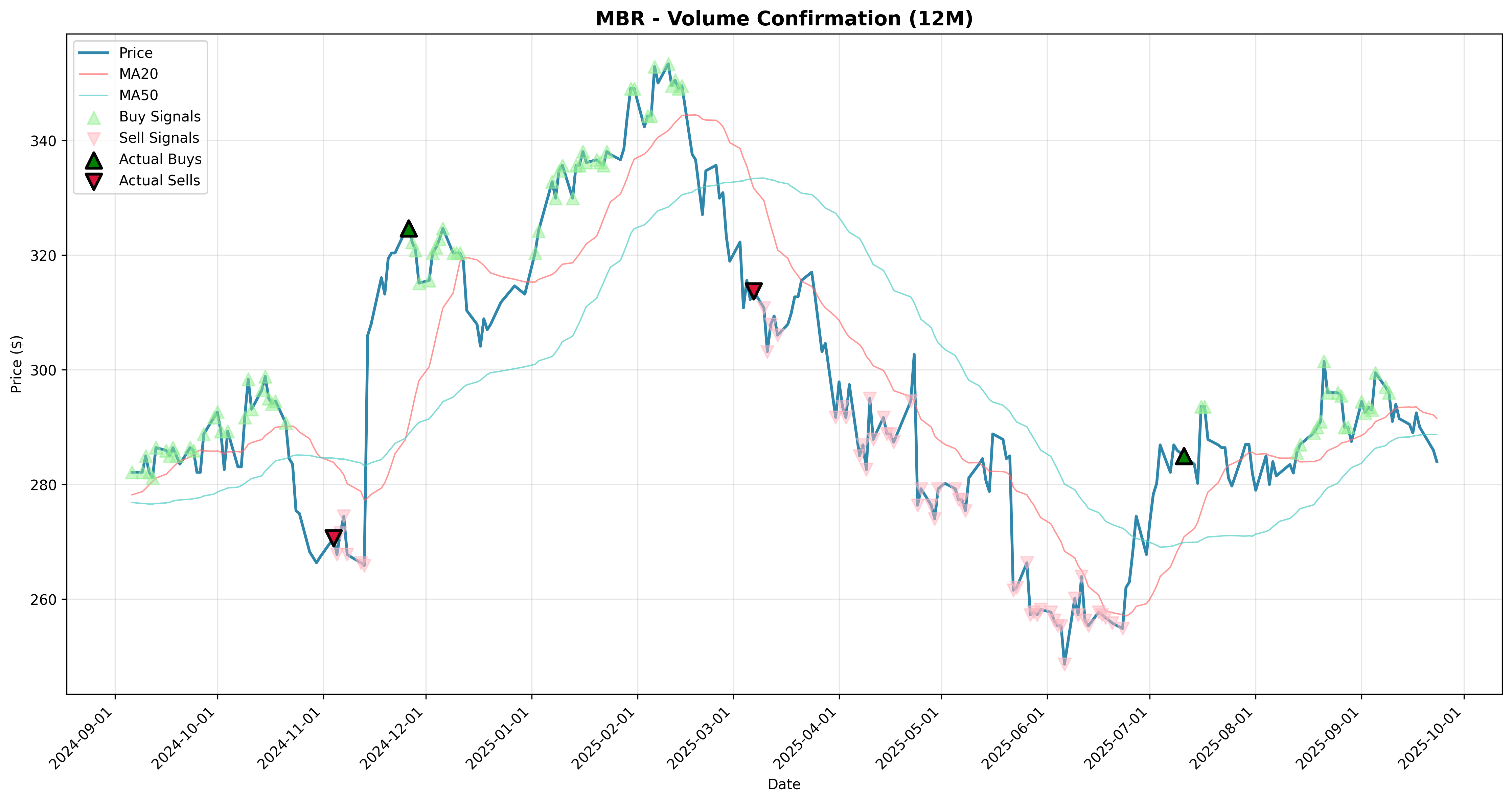

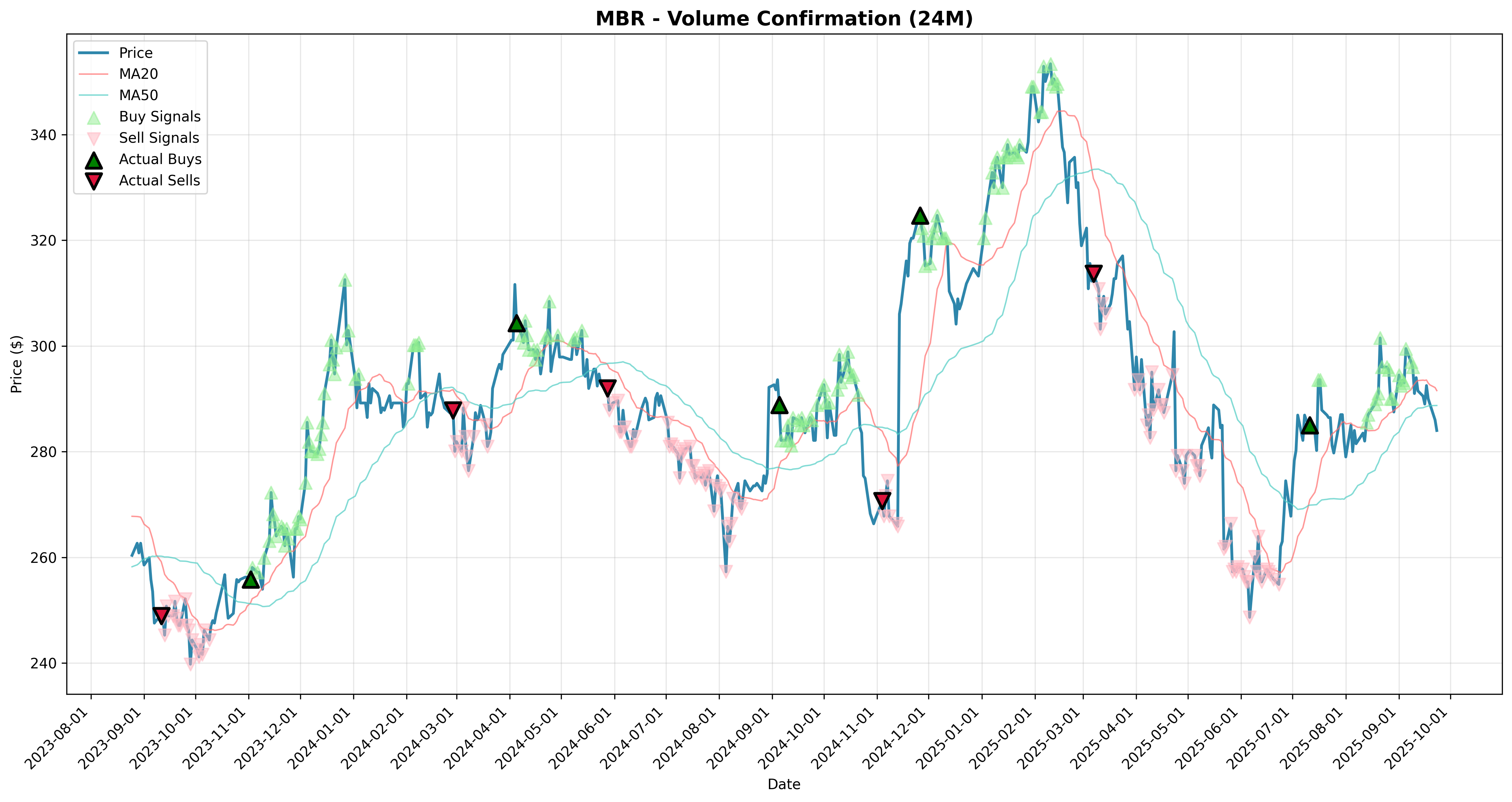

| volume_confirmation | MBR | 263.73% | -0.4% | -0.4% | -9.0% | -2.6% | -135.11% | 0.28 | -64.27% | 47 | 48.94% | $363,731 |

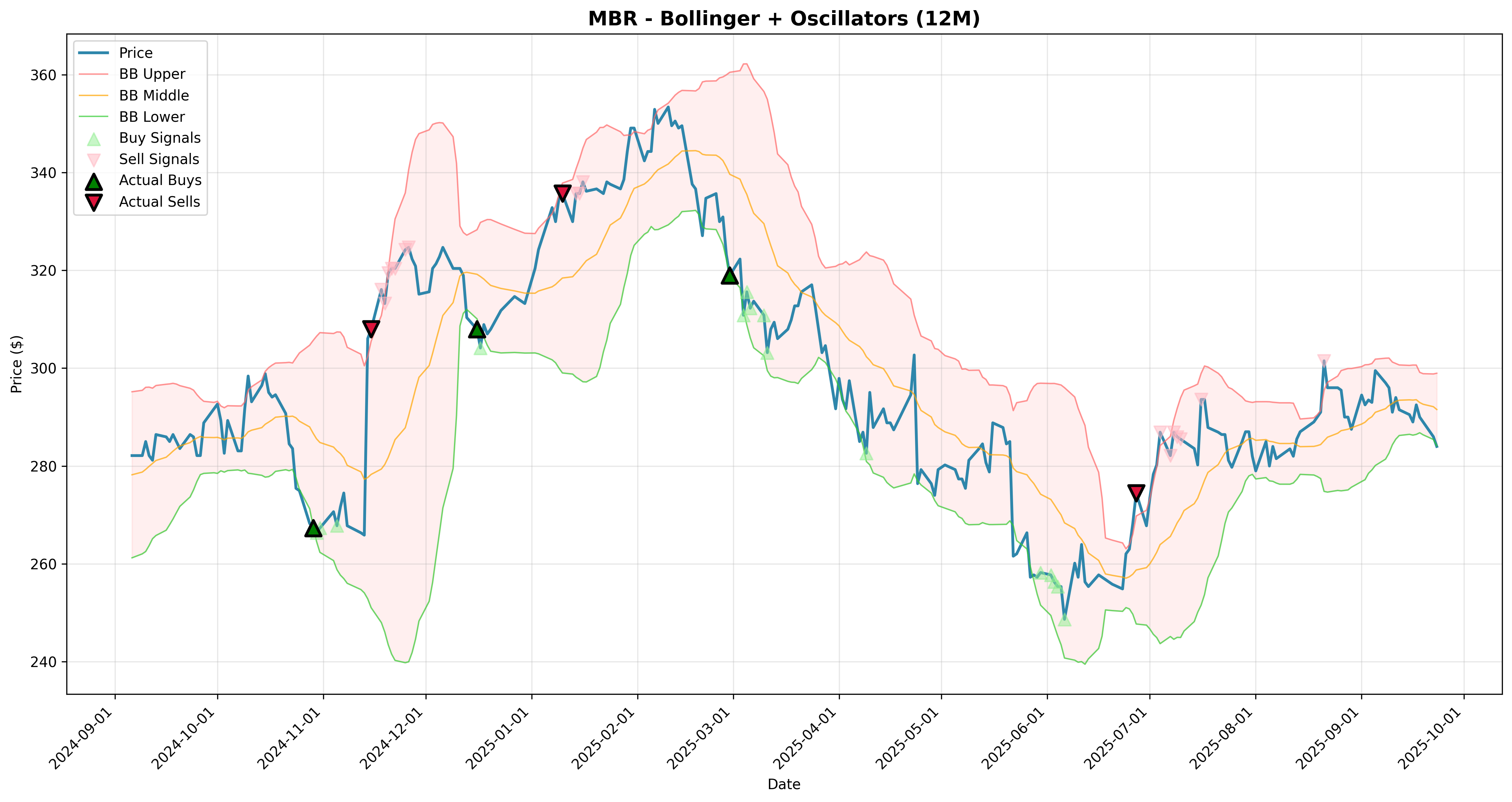

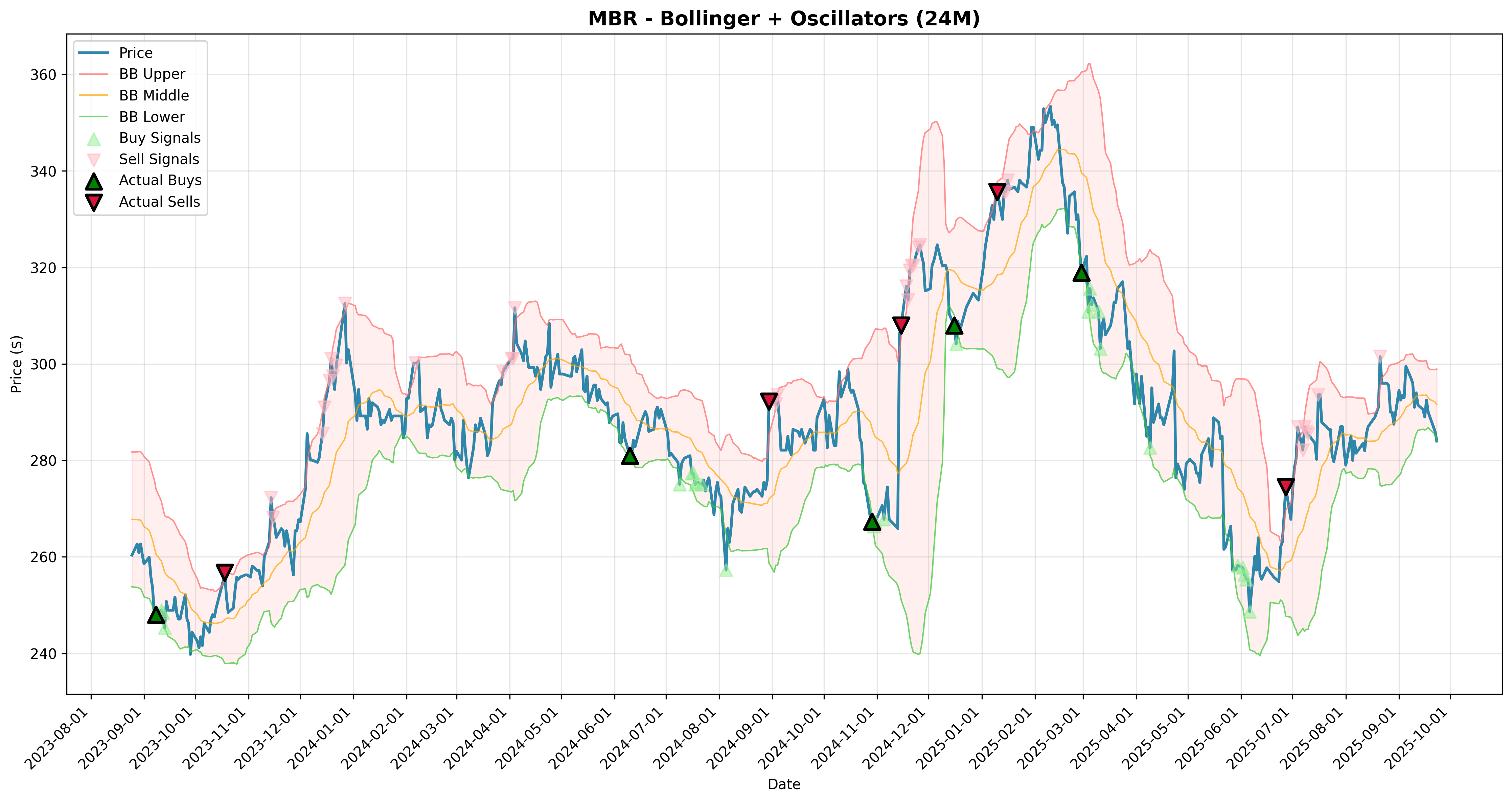

| bollinger_oscillators | MBR | -52.39% | 7.7% | -13.4% | 8.1% | 14.4% | -451.23% | -0.18 | -90.60% | 36 | 50.00% | $47,611 |

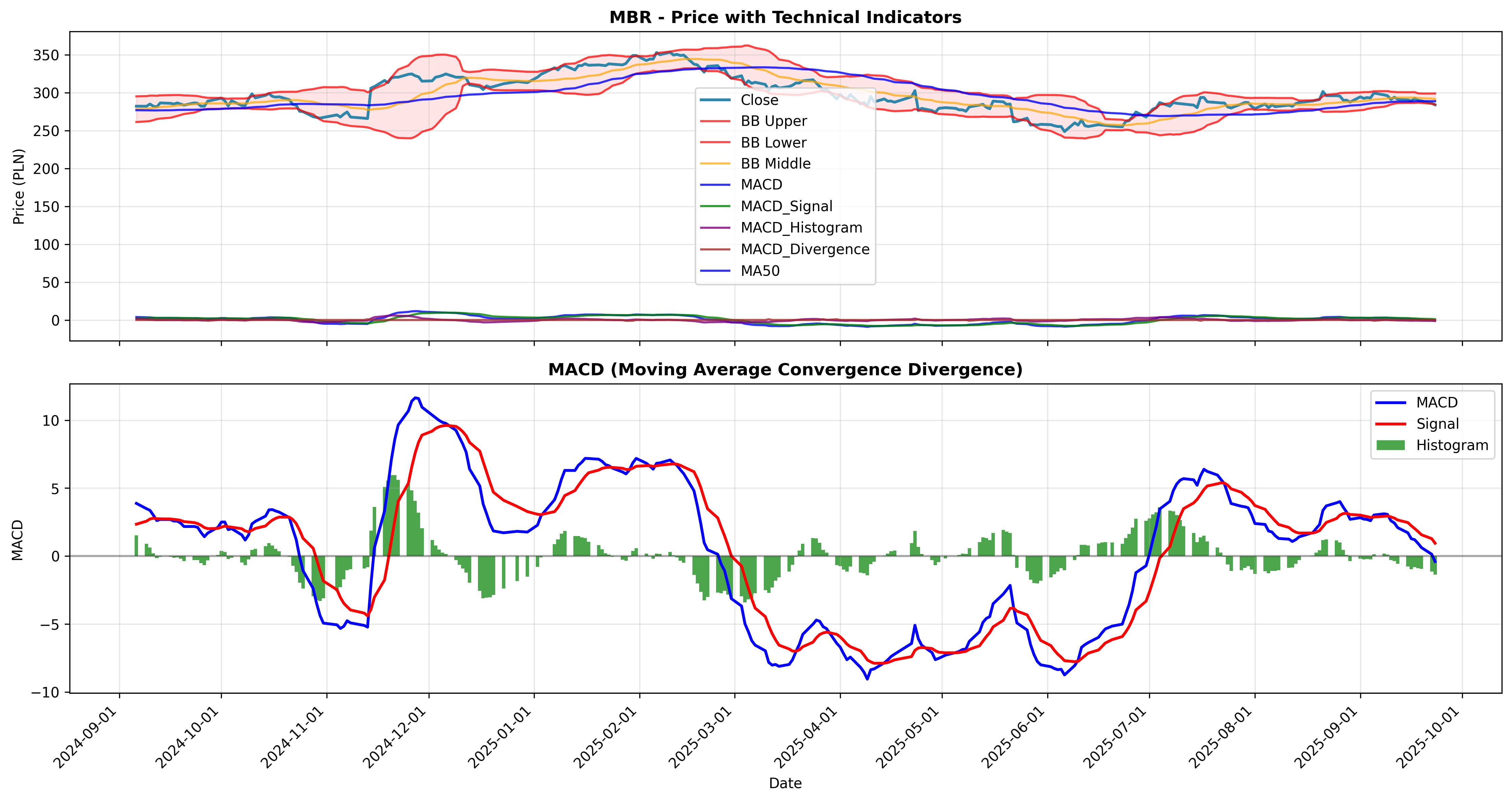

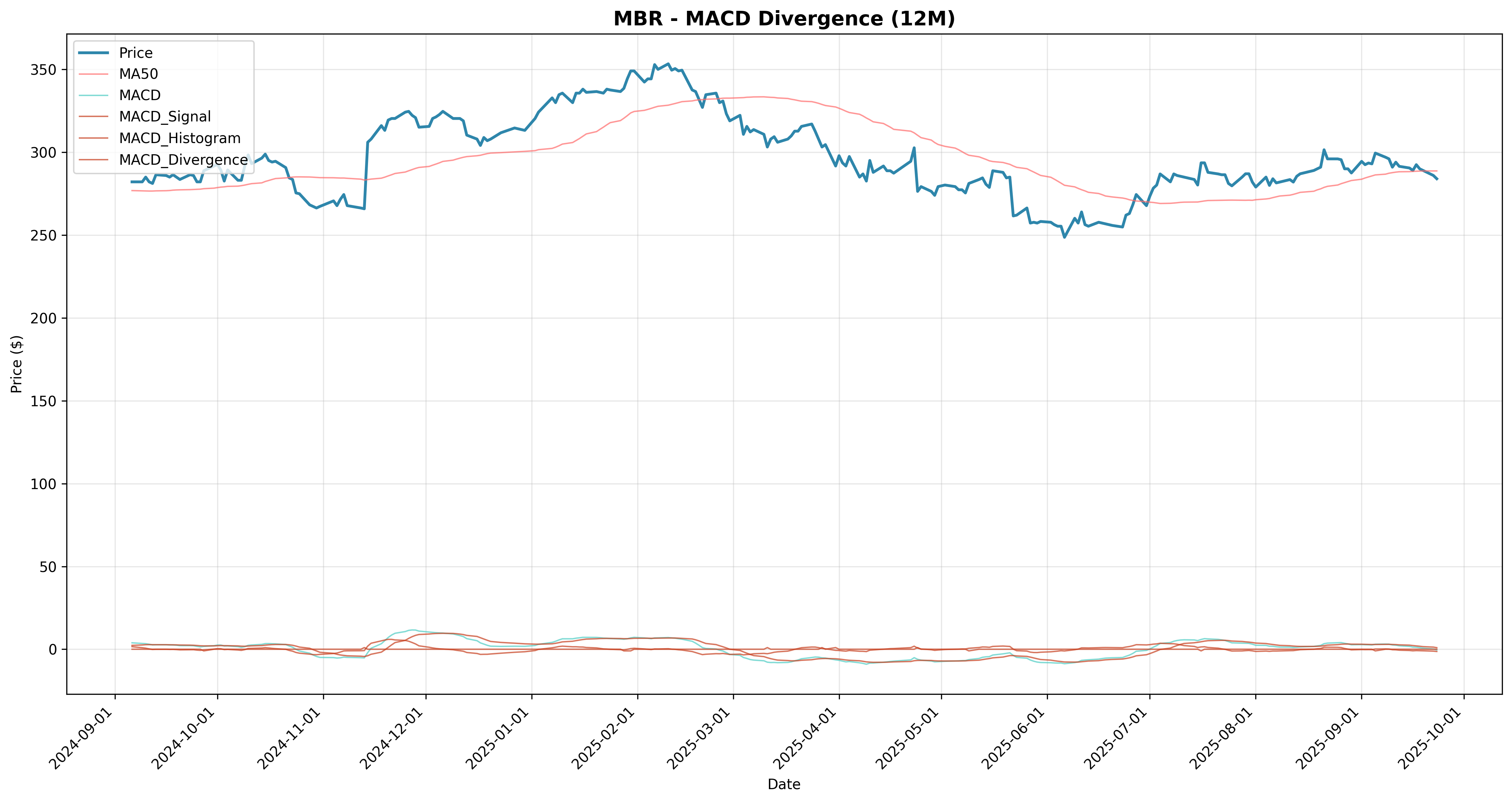

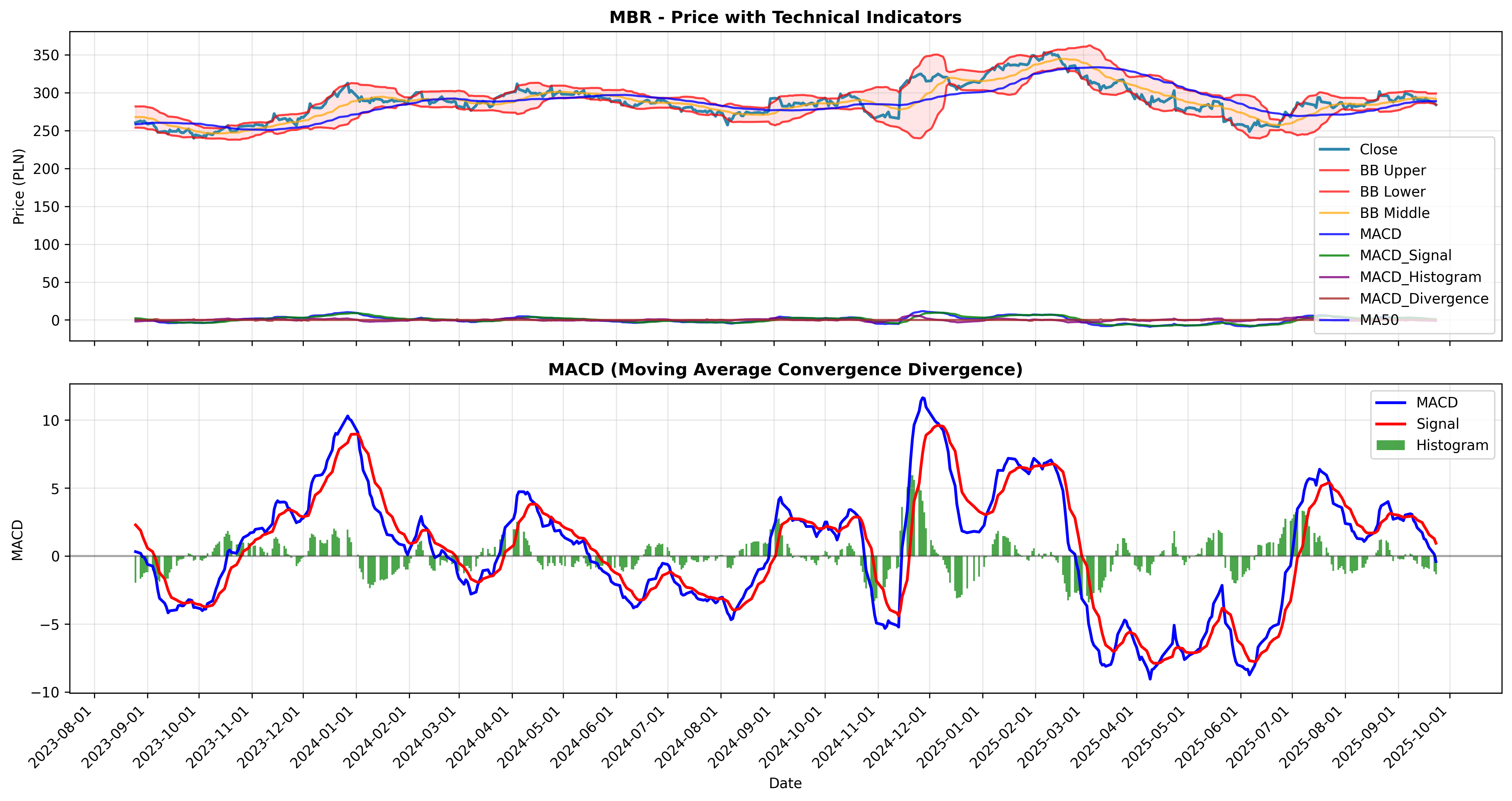

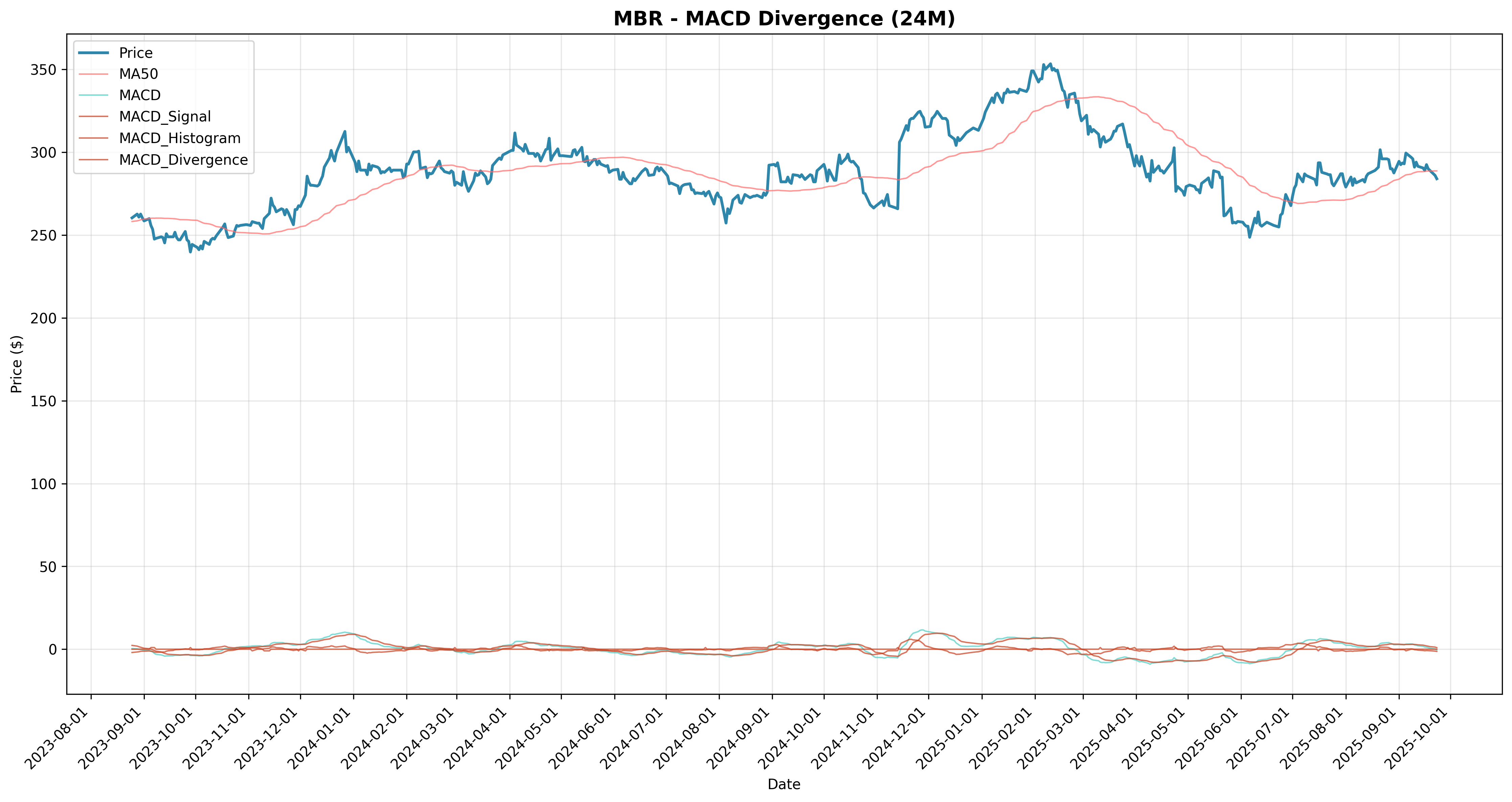

| macd_divergence | MBR | 0.00% | 0.0% | 0.0% | 0.0% | 0.0% | 0.00% | 0.00 | 0.00% | 0 | 0.00% | $100,000 |

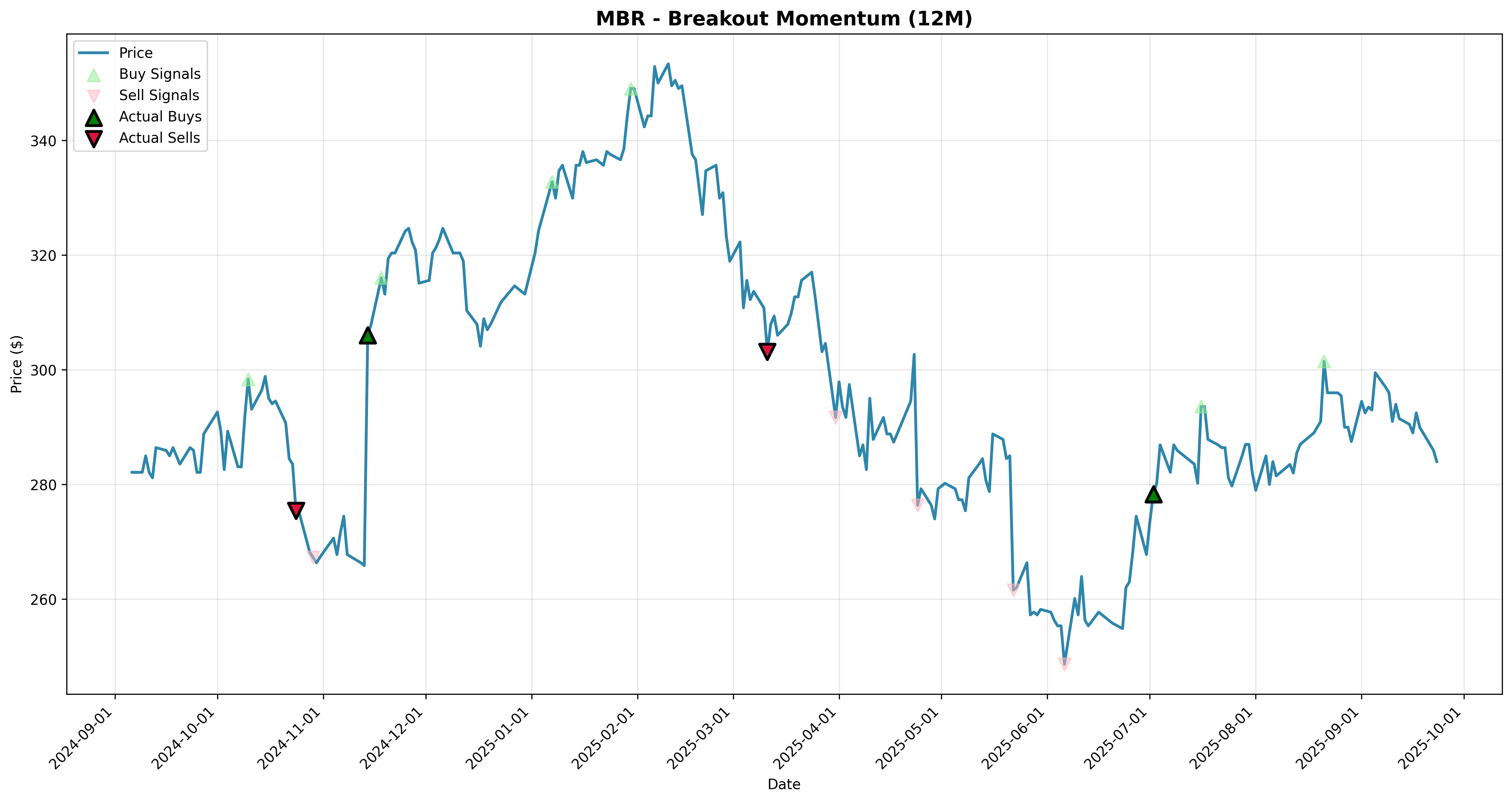

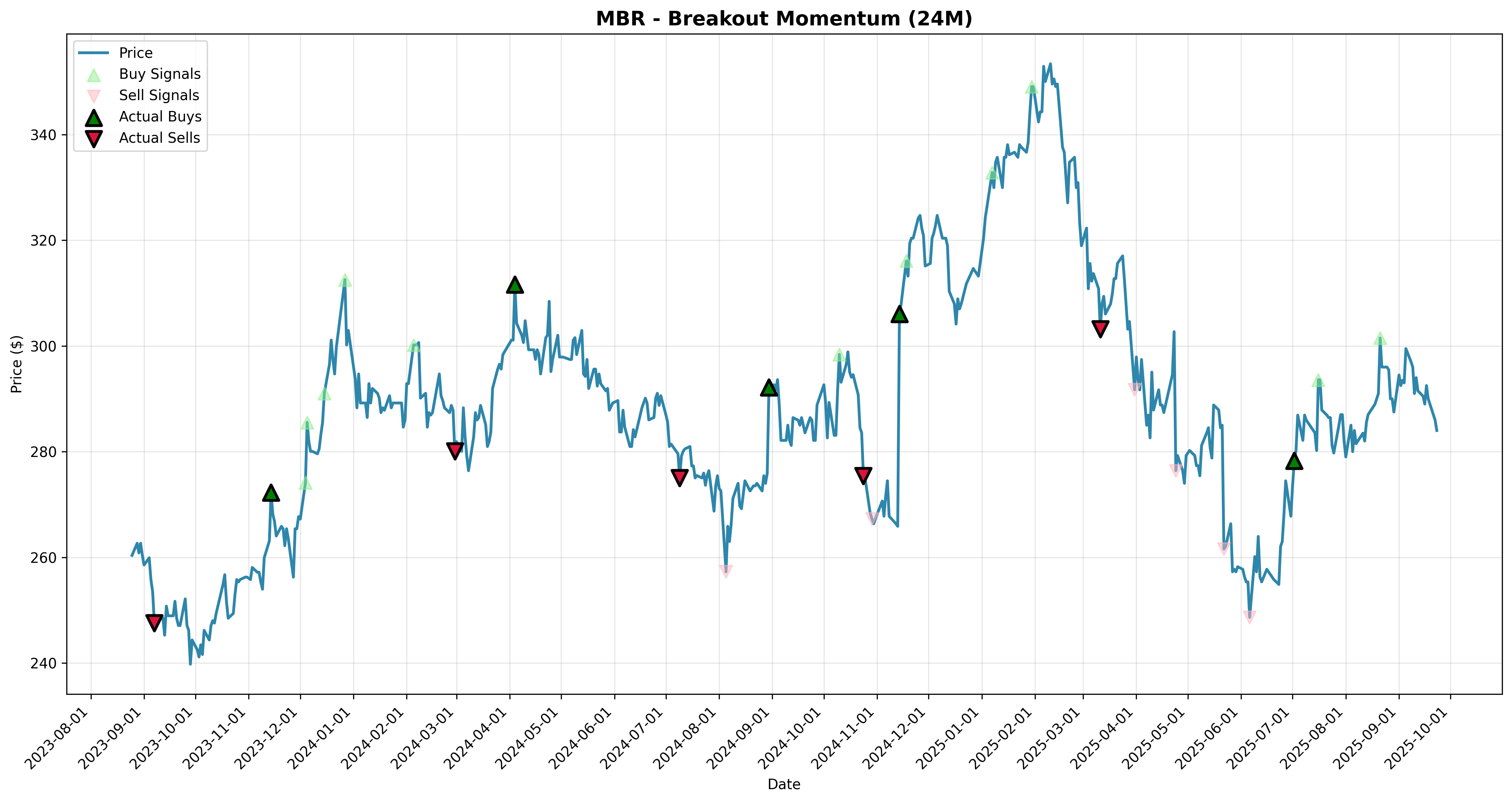

| breakout_momentum | MBR | 325.07% | 2.0% | 2.0% | -2.8% | -13.5% | -73.78% | 0.32 | -78.66% | 35 | 48.57% | $425,068 |

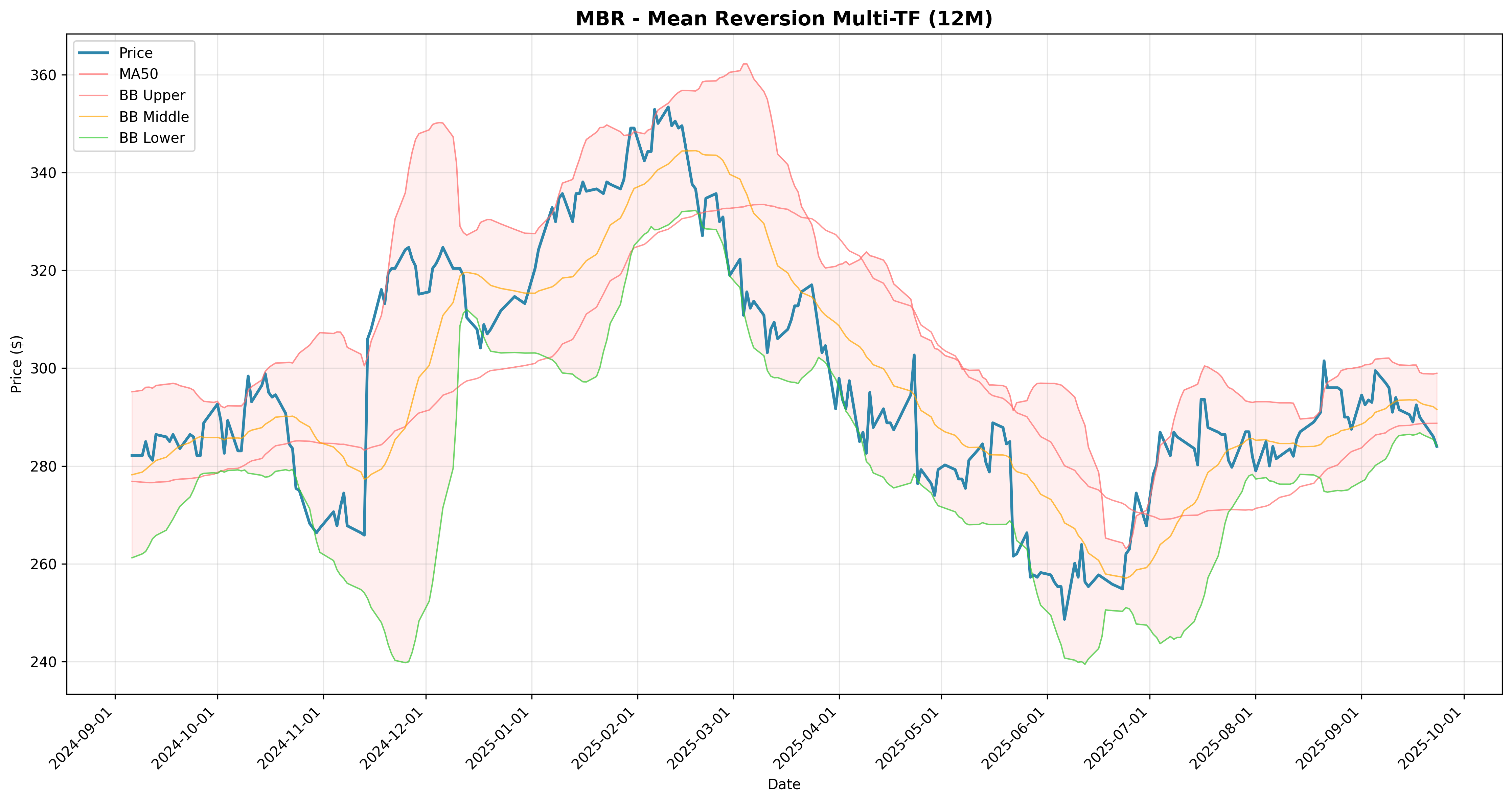

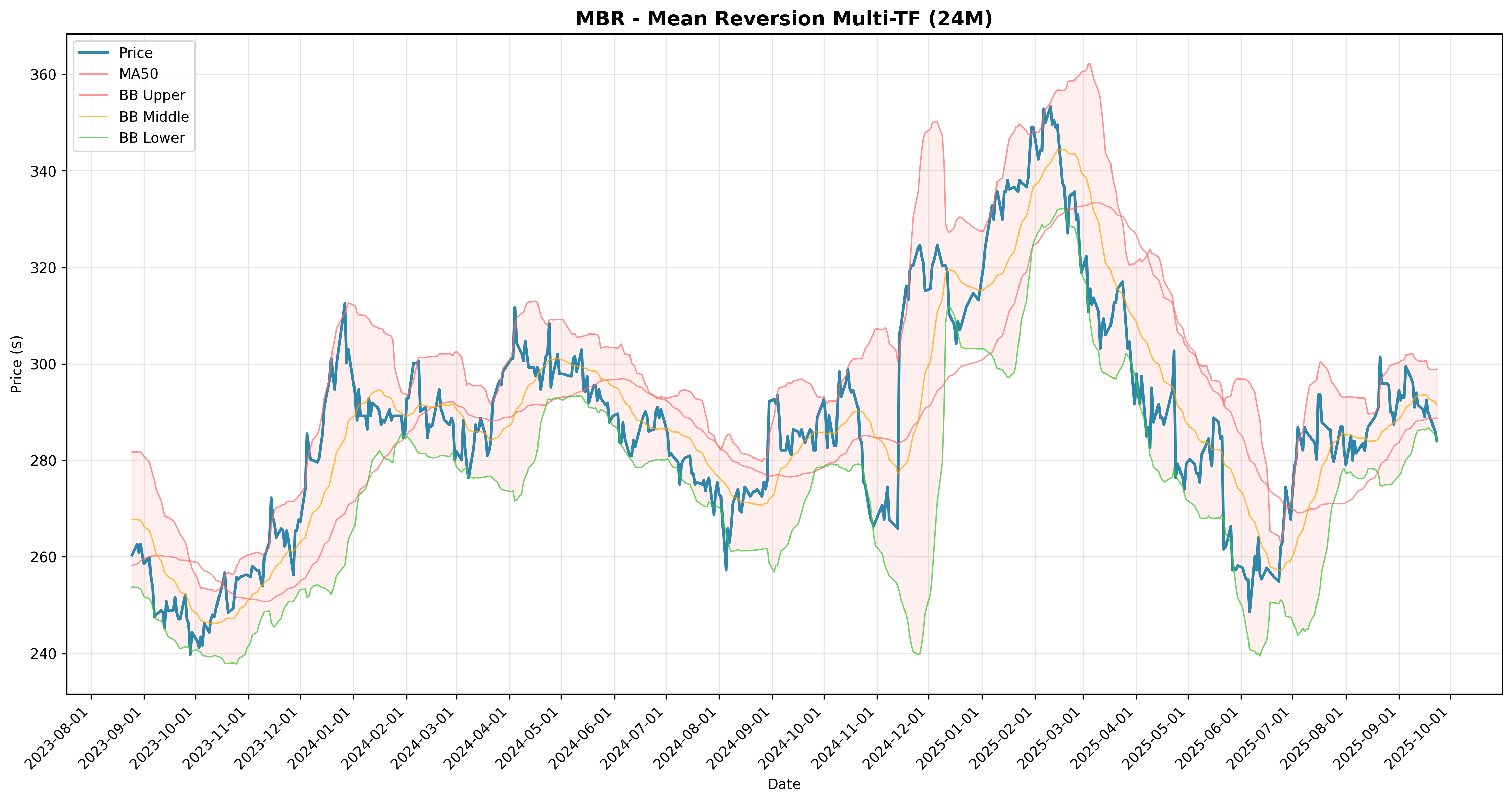

| mean_reversion_multi_tf | MBR | 0.00% | 0.0% | 0.0% | 0.0% | 0.0% | 0.00% | 0.00 | 0.00% | 0 | 0.00% | $100,000 |

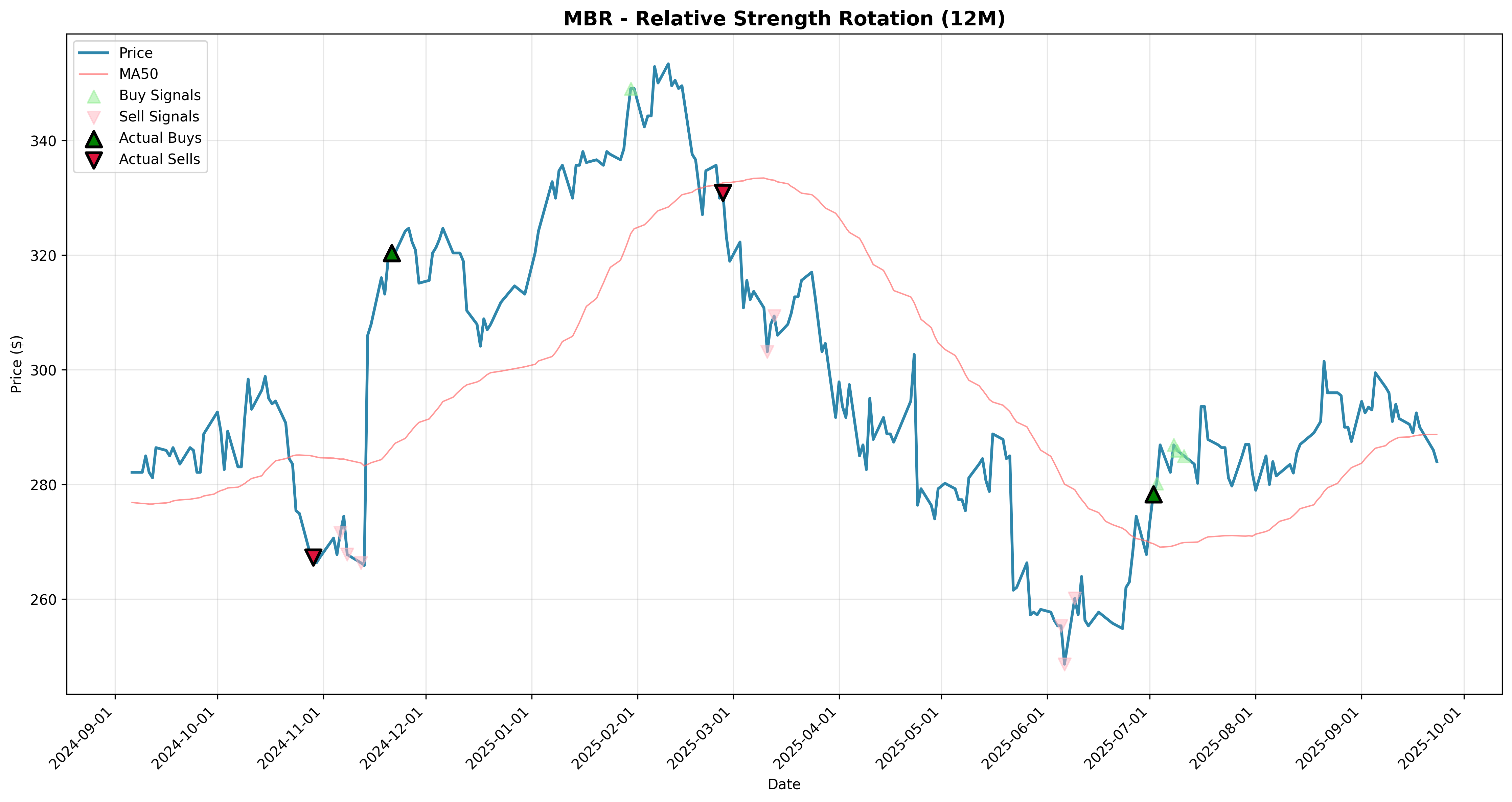

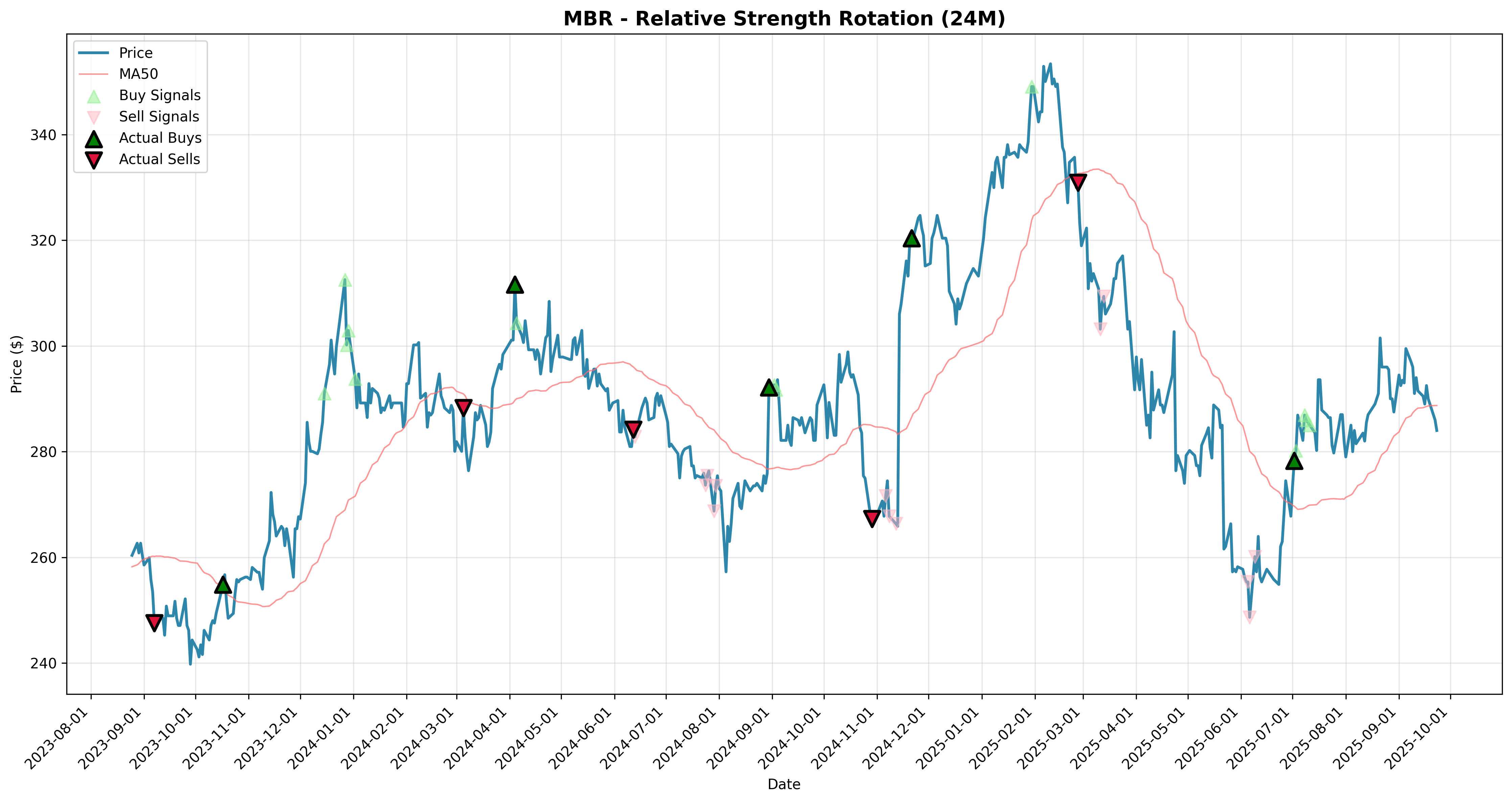

| relative_strength_rotation | MBR | 928.82% | 2.0% | 2.0% | -1.6% | -0.5% | 529.98% | 0.57 | -50.96% | 35 | 48.57% | $1,028,823 |

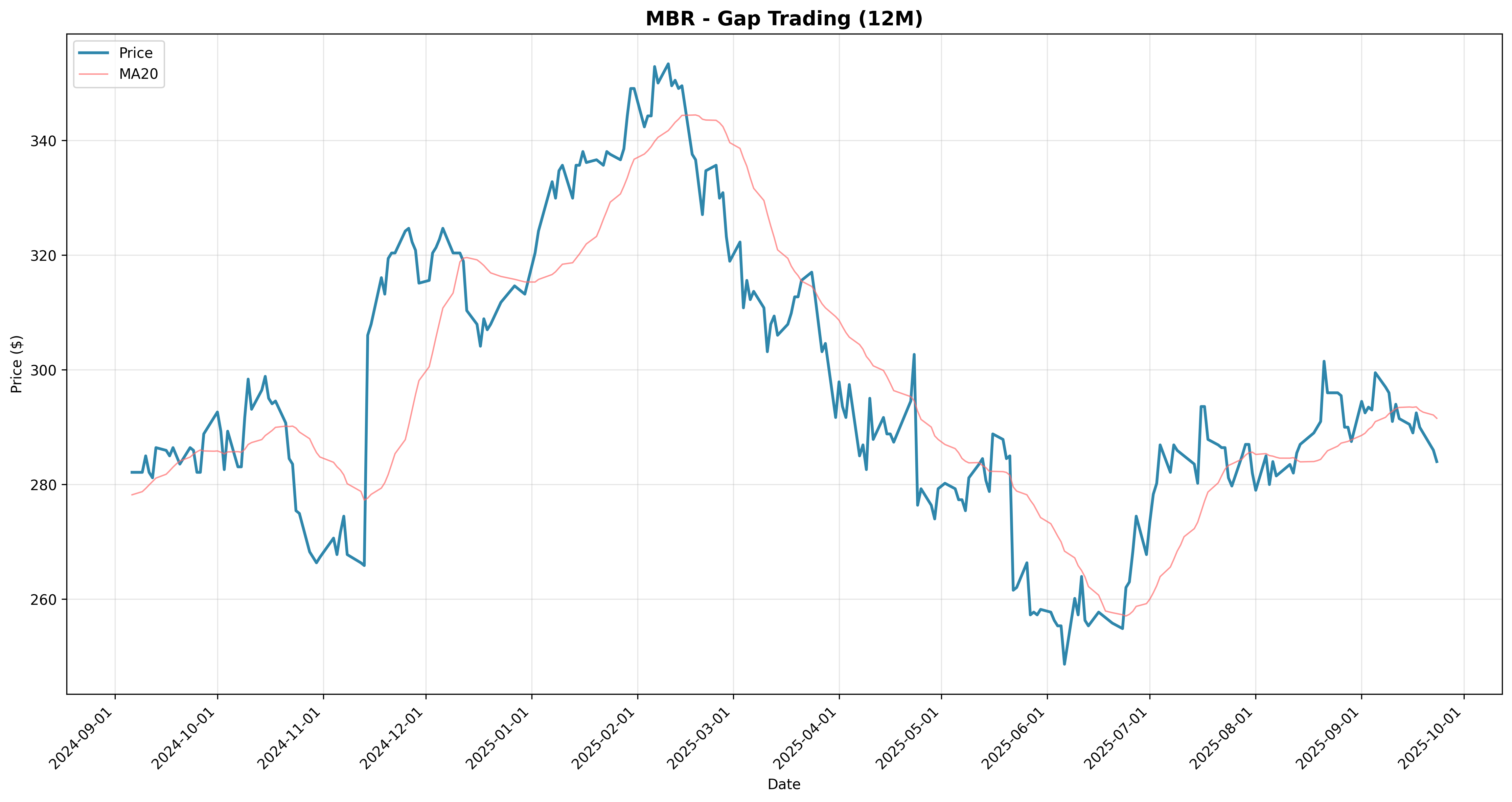

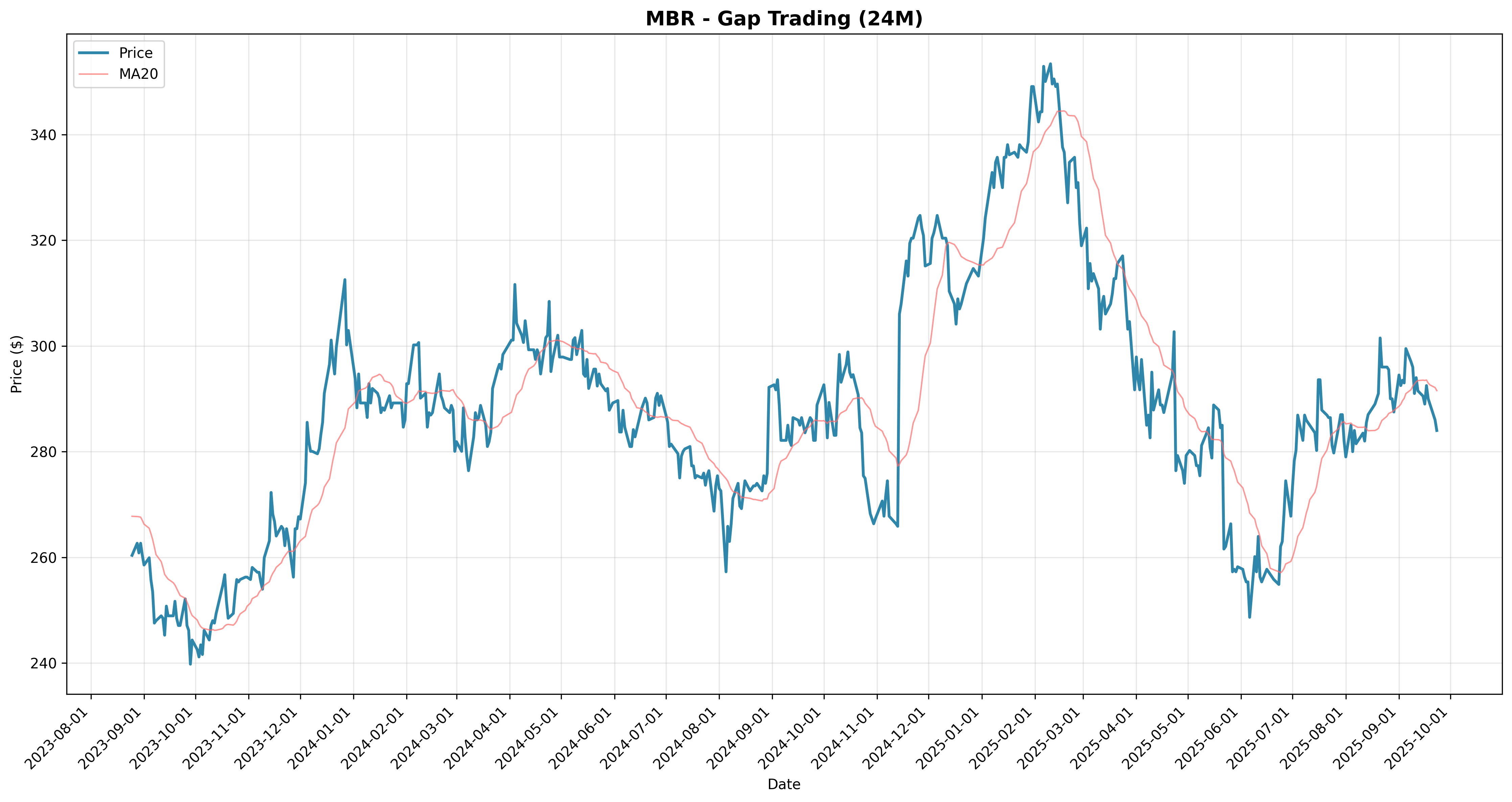

| gap_trading | MBR | 2889.35% | 11.4% | -10.4% | -0.9% | 12.6% | 2490.50% | 0.00 | 0.00% | 1 | 0.00% | $2,989,348 |

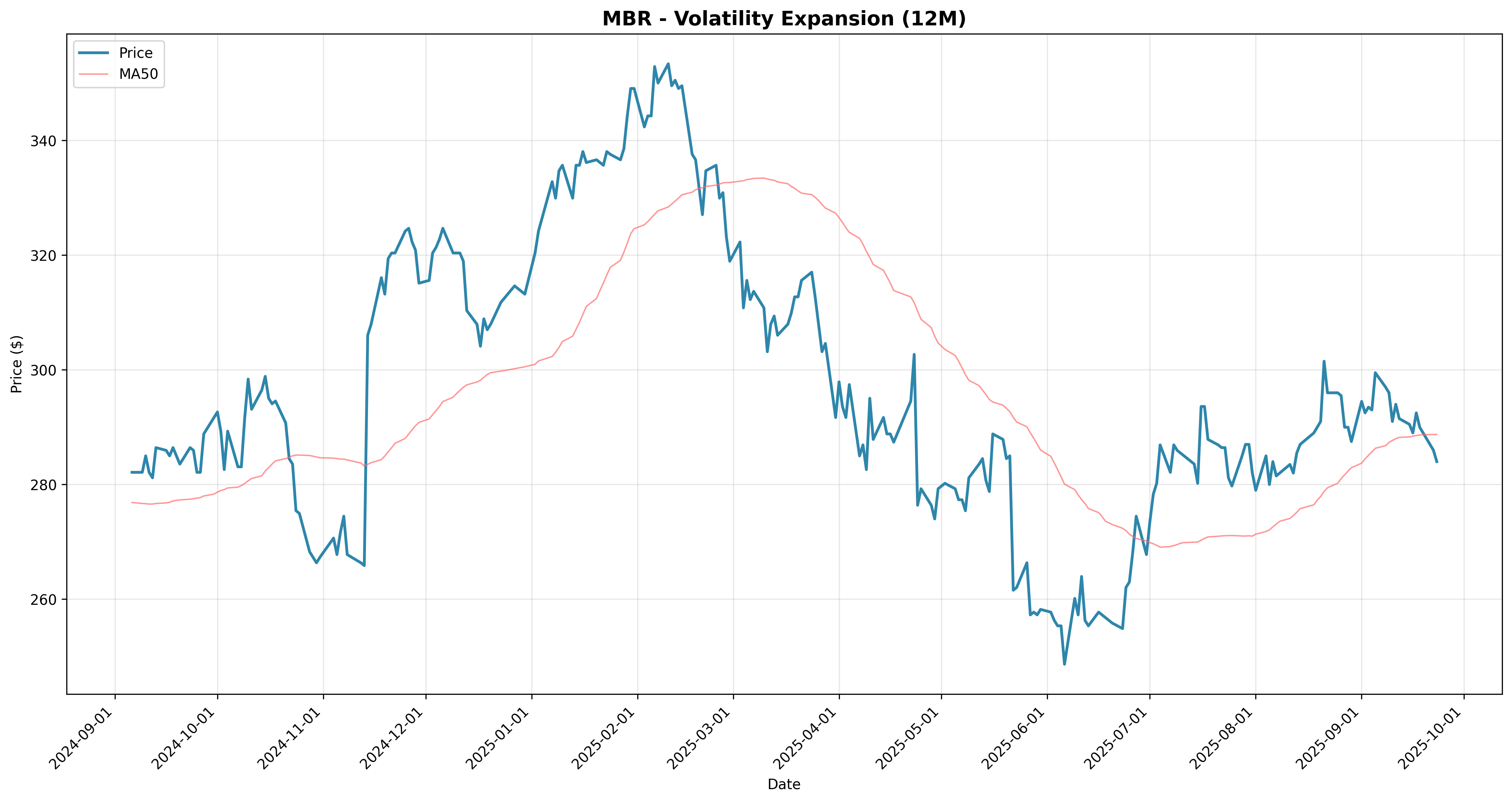

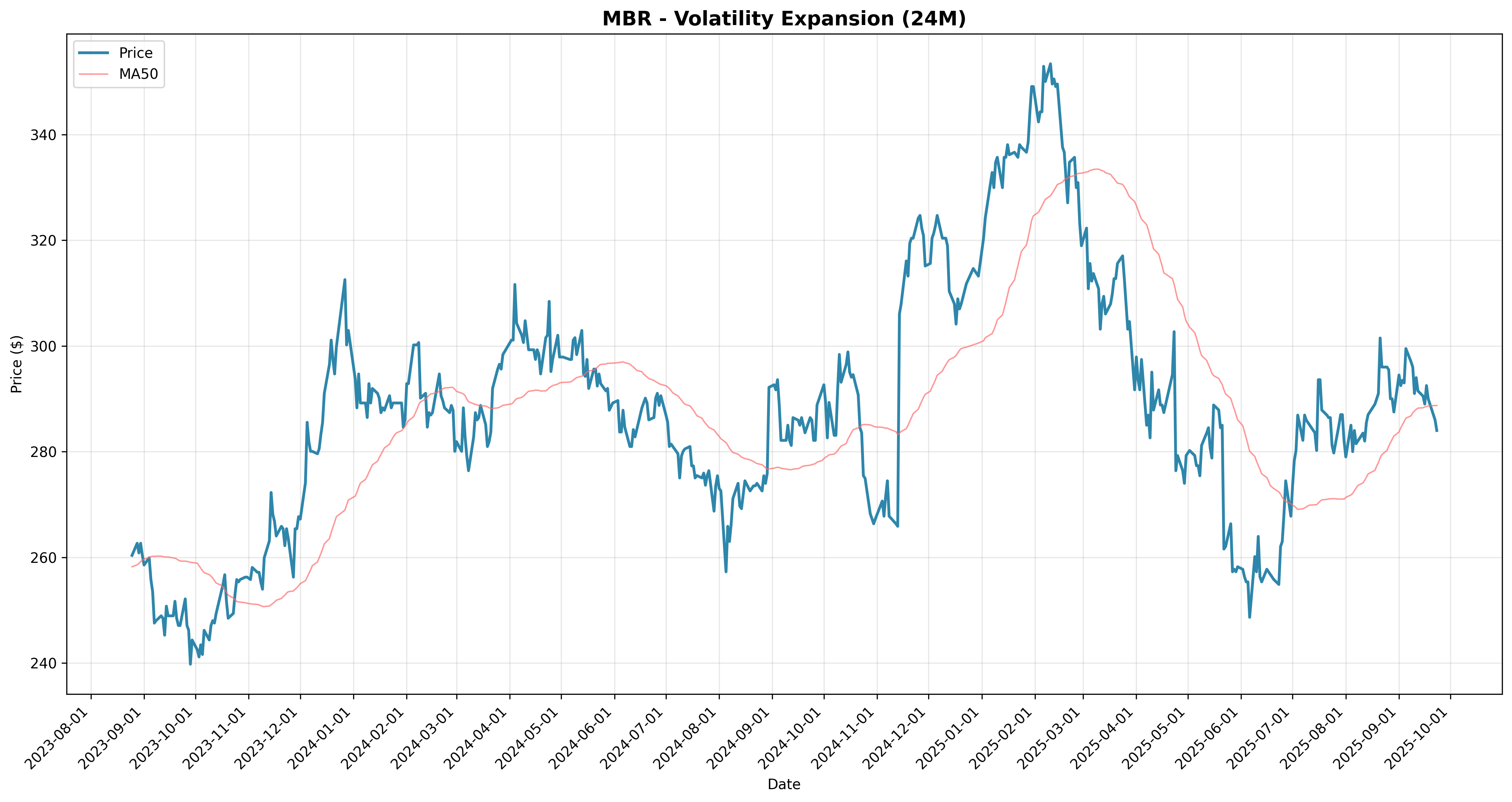

| volatility_expansion | MBR | 1335.47% | 0.0% | 0.0% | 0.0% | 0.0% | 936.63% | 0.60 | -73.36% | 2 | 50.00% | $1,435,474 |

| momentum_kirkpatrick | MBR | 282.77% | 2.4% | -6.5% | -12.6% | -13.0% | -116.07% | 0.34 | -75.48% | 134 | 50.00% | $382,772 |

Best Strategy: gap_trading

- Symbol: MBR

- Total Return: 2889.35%

- Sharpe Ratio: 0.00

- Max Drawdown: 0.00%

- Final Portfolio Value: $2,989,348

Key Metrics

- Initial Capital: $100,000

- Analysis Date: 2025-09-24

- Portfolio Manager: Active (Extreme returns fix applied)

Period Analysis

This report includes period-based return analysis for the following timeframes:

- 3M Return: Performance over the last 3 months

- 6M Return: Performance over the last 6 months

- 12M Return: Performance over the last 12 months

- 24M Return: Performance over the last 24 months

Period-based analysis helps identify strategy behavior across different market conditions and time horizons.

Recent Trading Signals

📊 Today’s Signals (2025-09-24)

⚪ No new trading signals detected in today’s analysis.

📈 Most Recent Signals by Strategy

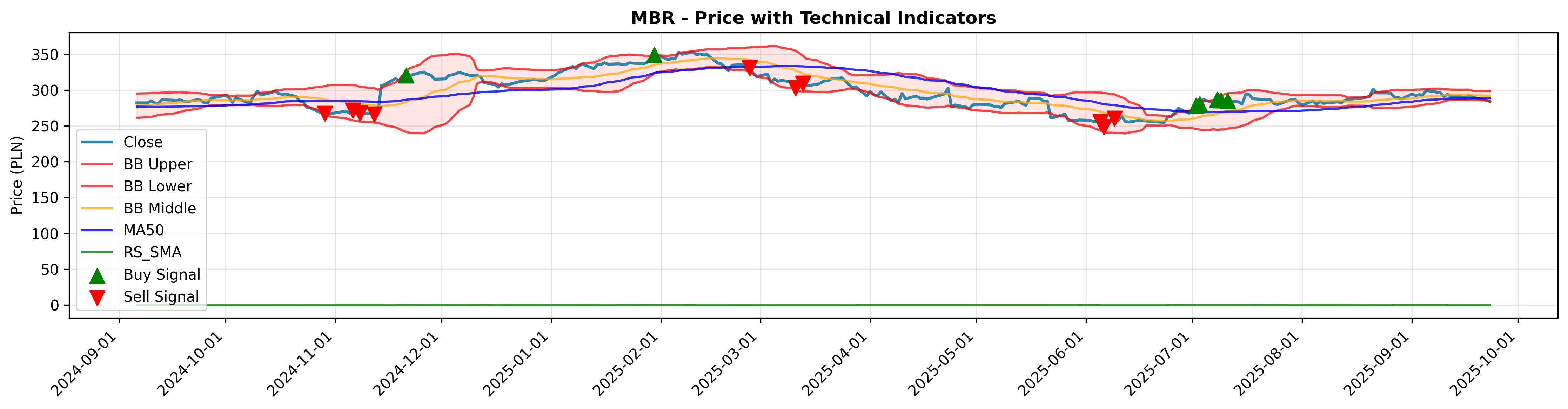

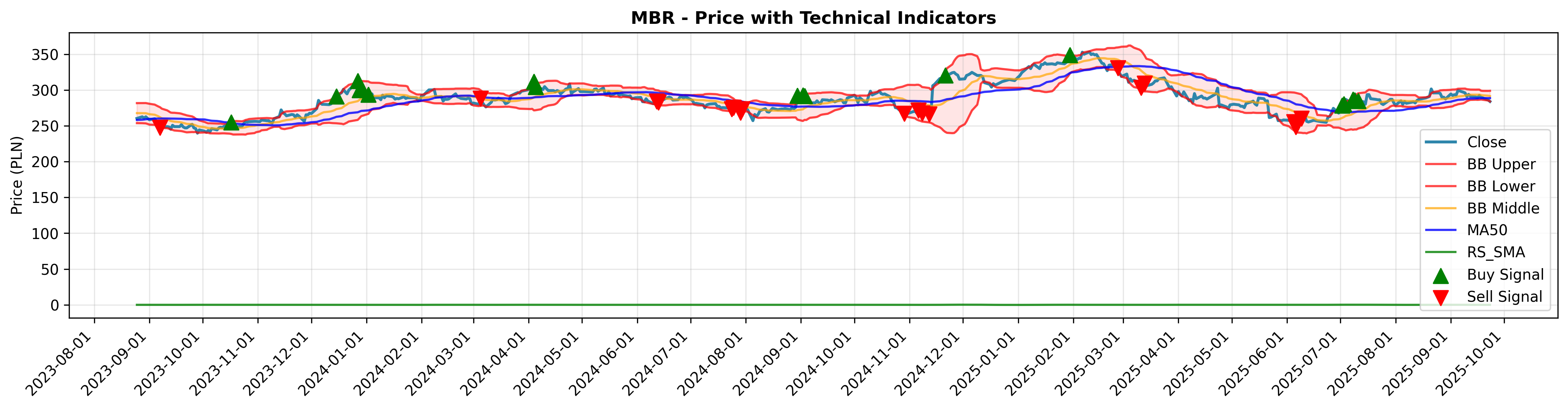

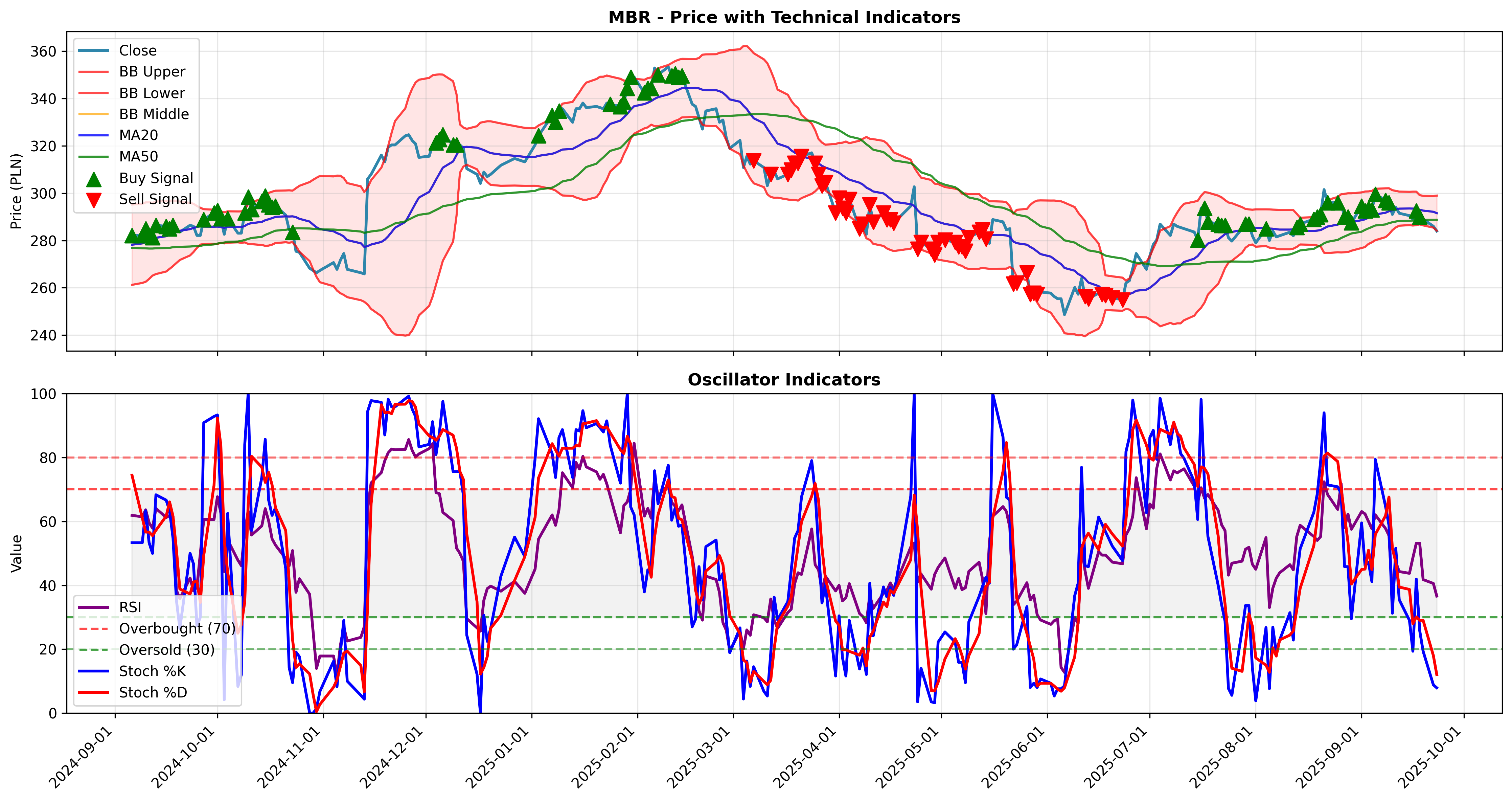

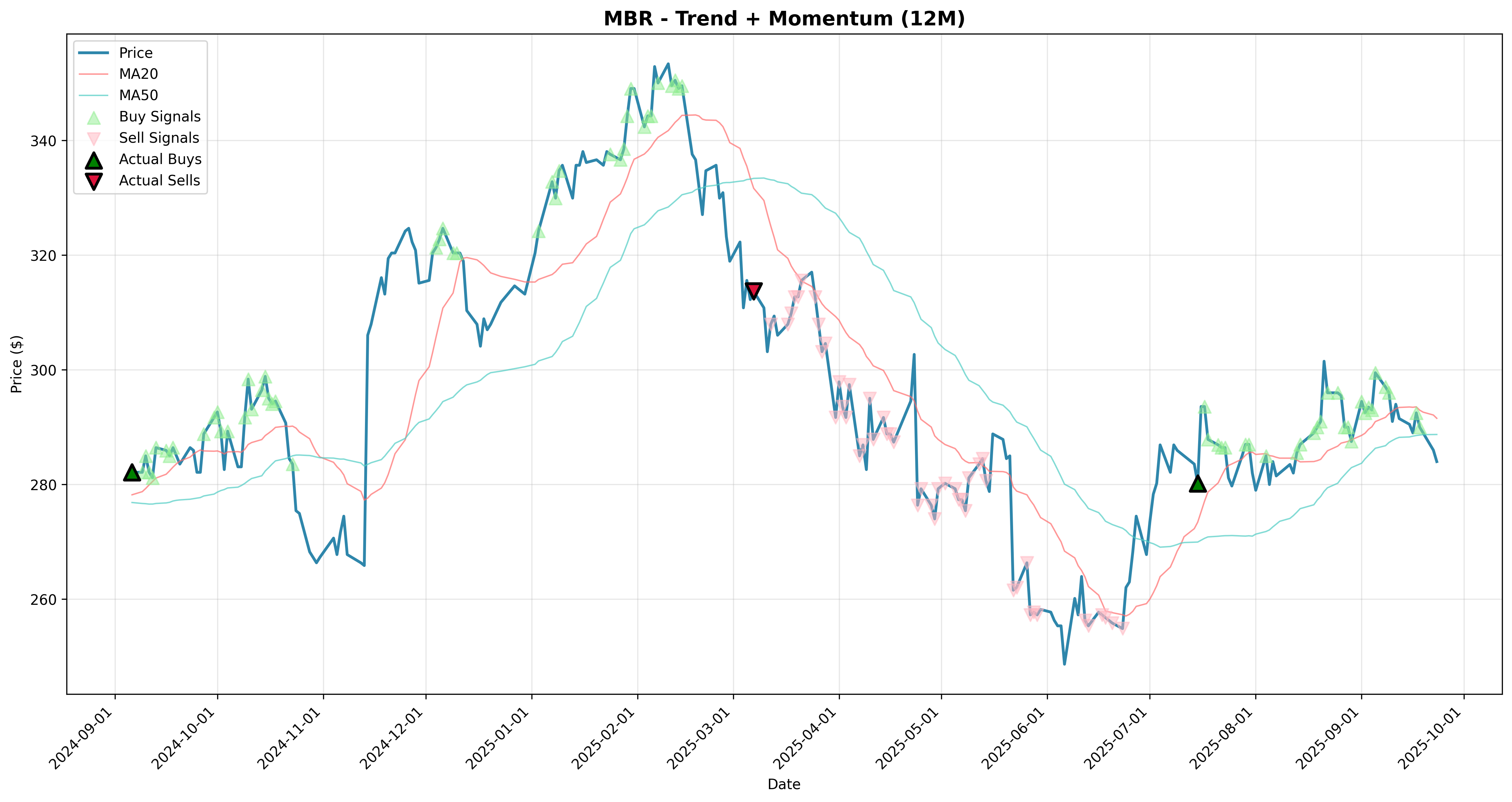

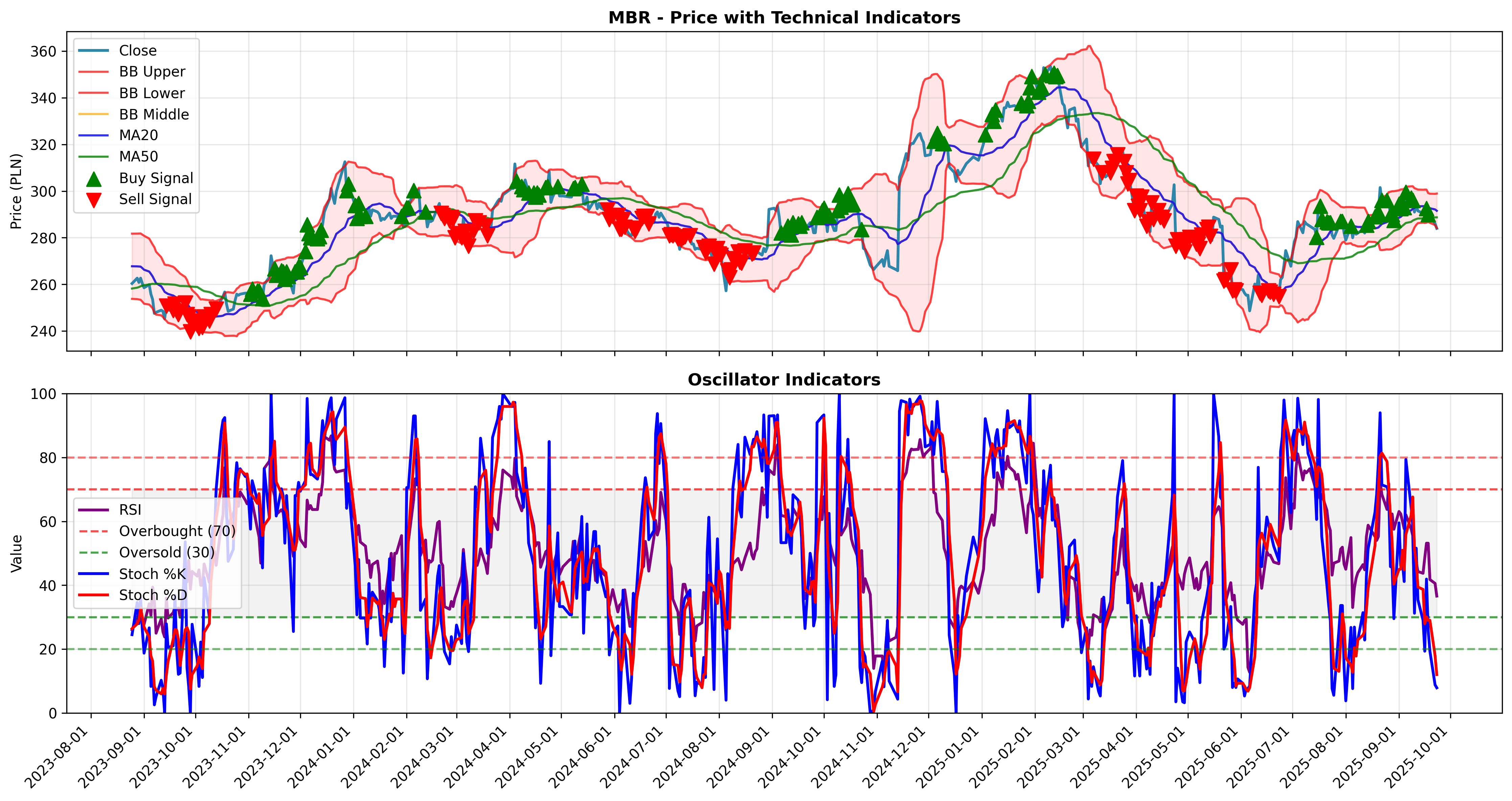

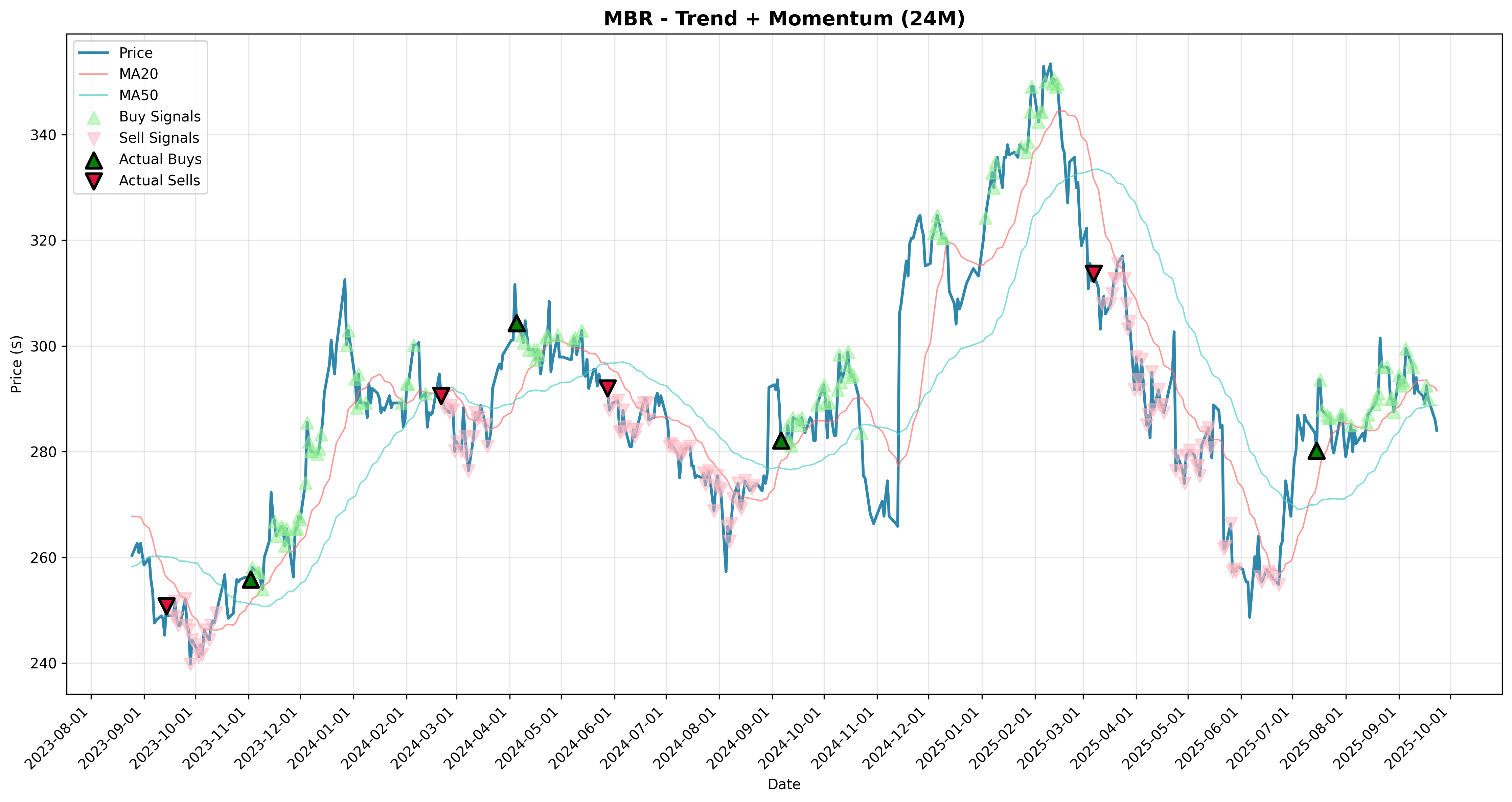

🟢 Trend Momentum: Last BUY on 2025-09-18

- 📊 Total Confidence: 20.3%

- 🟢 Composite: 24.8%

- 🔵 Conservative: 0.0%

- 🔴 Aggressive: 20.9%

- 🟡 Institutional: 25.7%

- 🟣 Quantitative: 30.2%

🟢 Dow Theory: Last BUY on 2016-03-01

- 📊 Total Confidence: 31.3%

- 🟢 Composite: 14.3%

- 🔵 Conservative: 21.4%

- 🔴 Aggressive: 17.1%

- 🟡 Institutional: 53.6%

- 🟣 Quantitative: 50.1%

🟢 Volume Confirmation: Last BUY on 2025-09-09

- 📊 Total Confidence: 17.7%

- 🟢 Composite: 21.7%

- 🔵 Conservative: 0.0%

- 🔴 Aggressive: 18.1%

- 🟡 Institutional: 22.3%

- 🟣 Quantitative: 26.3%

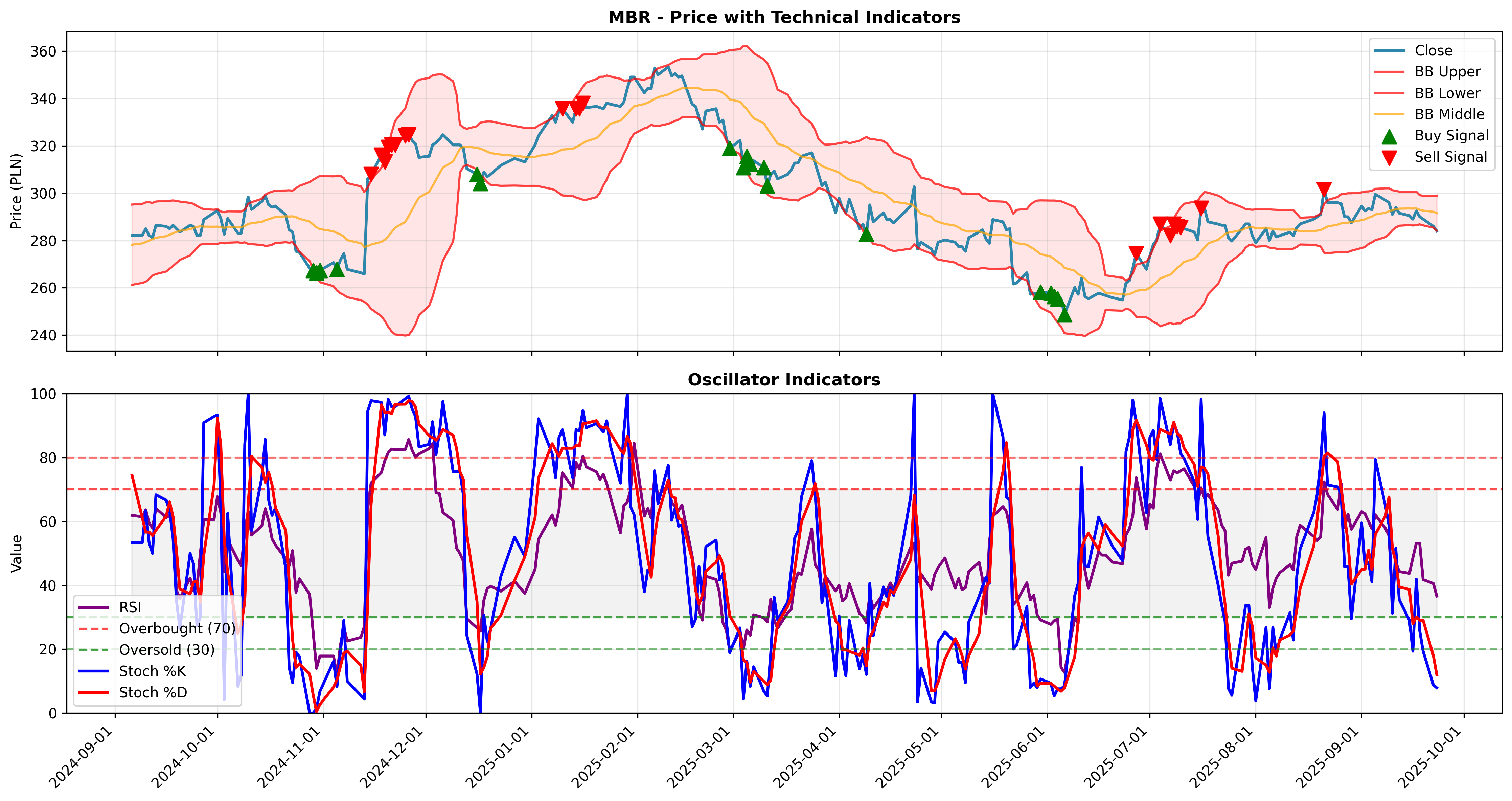

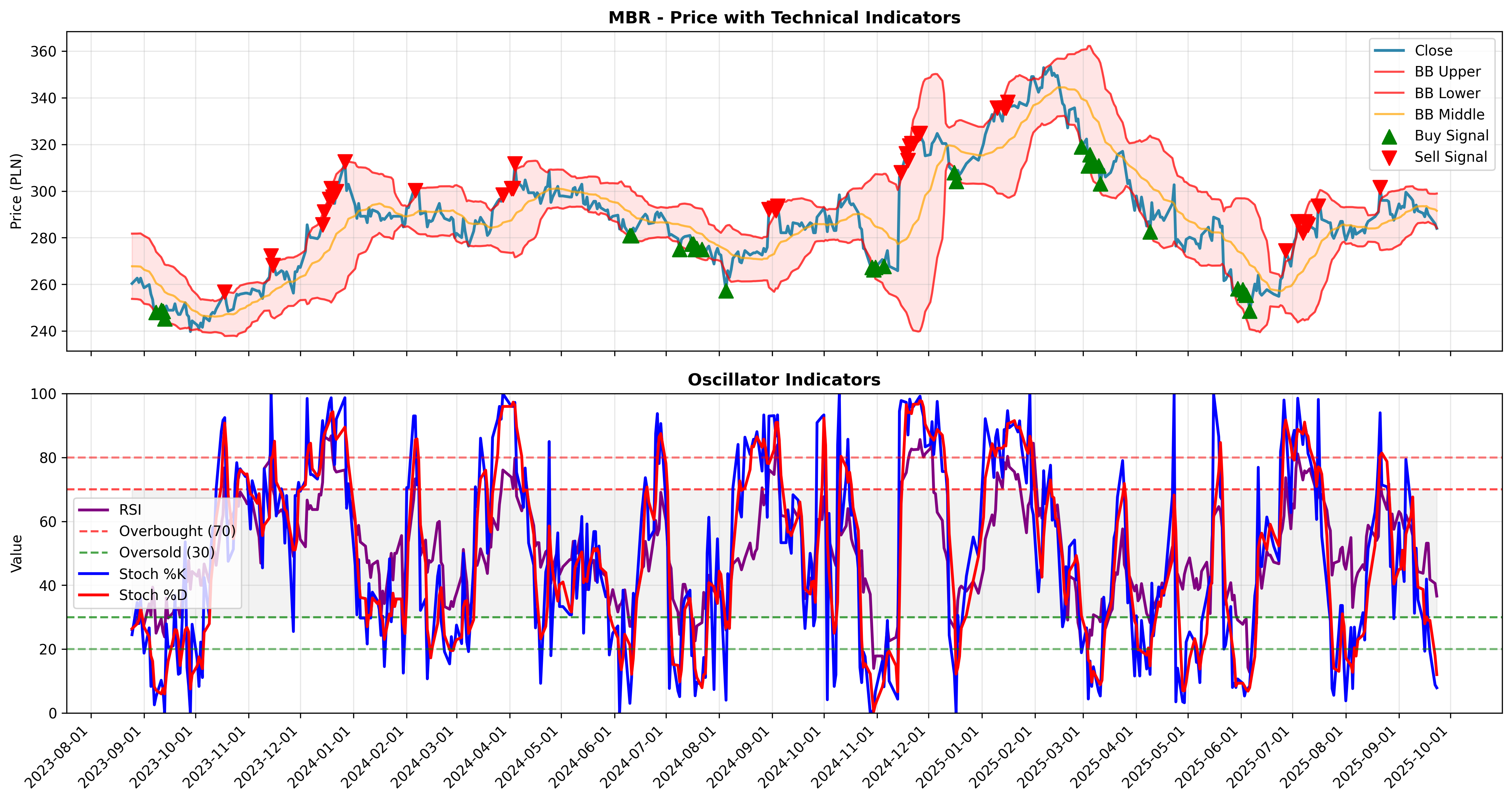

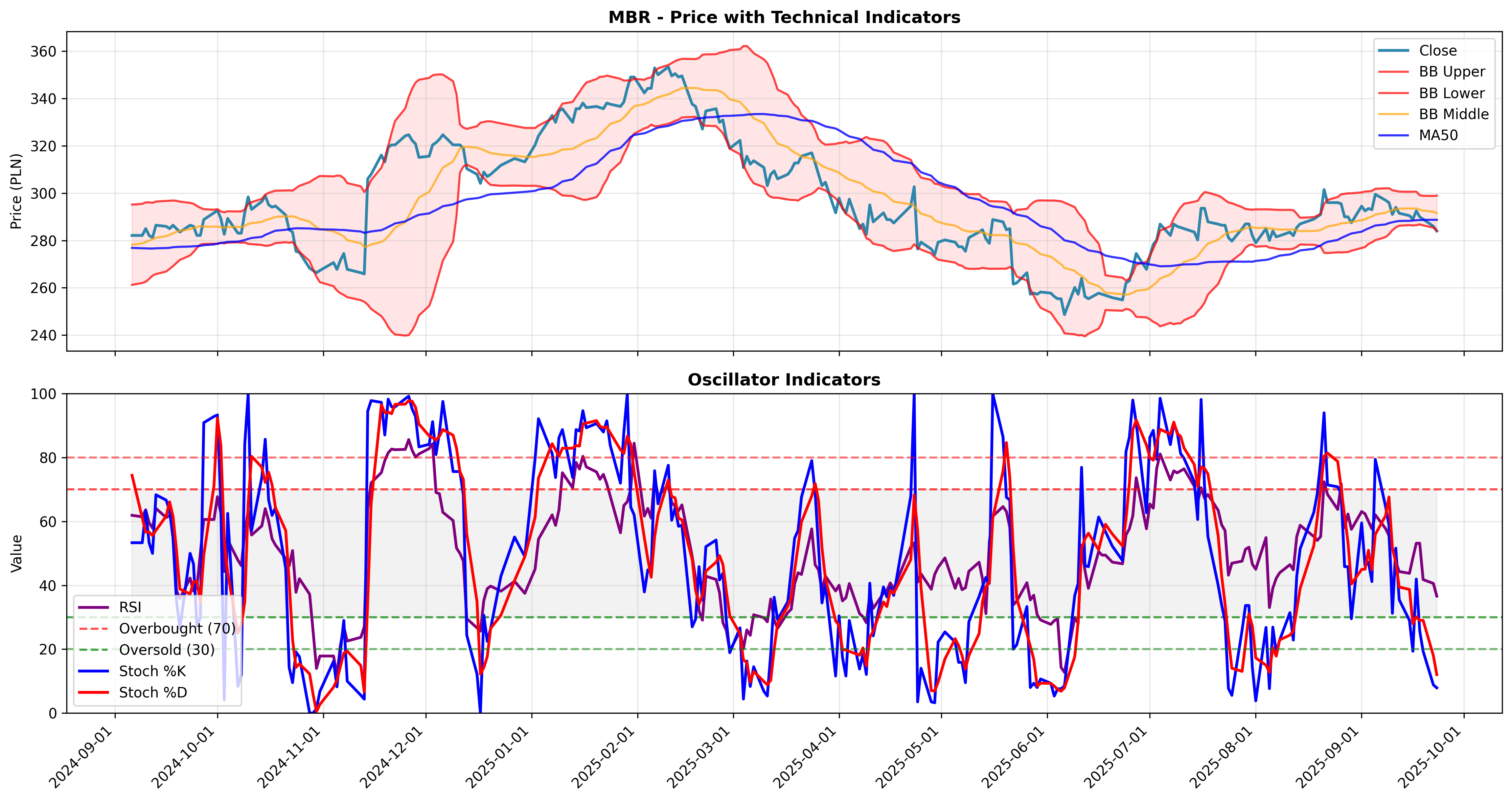

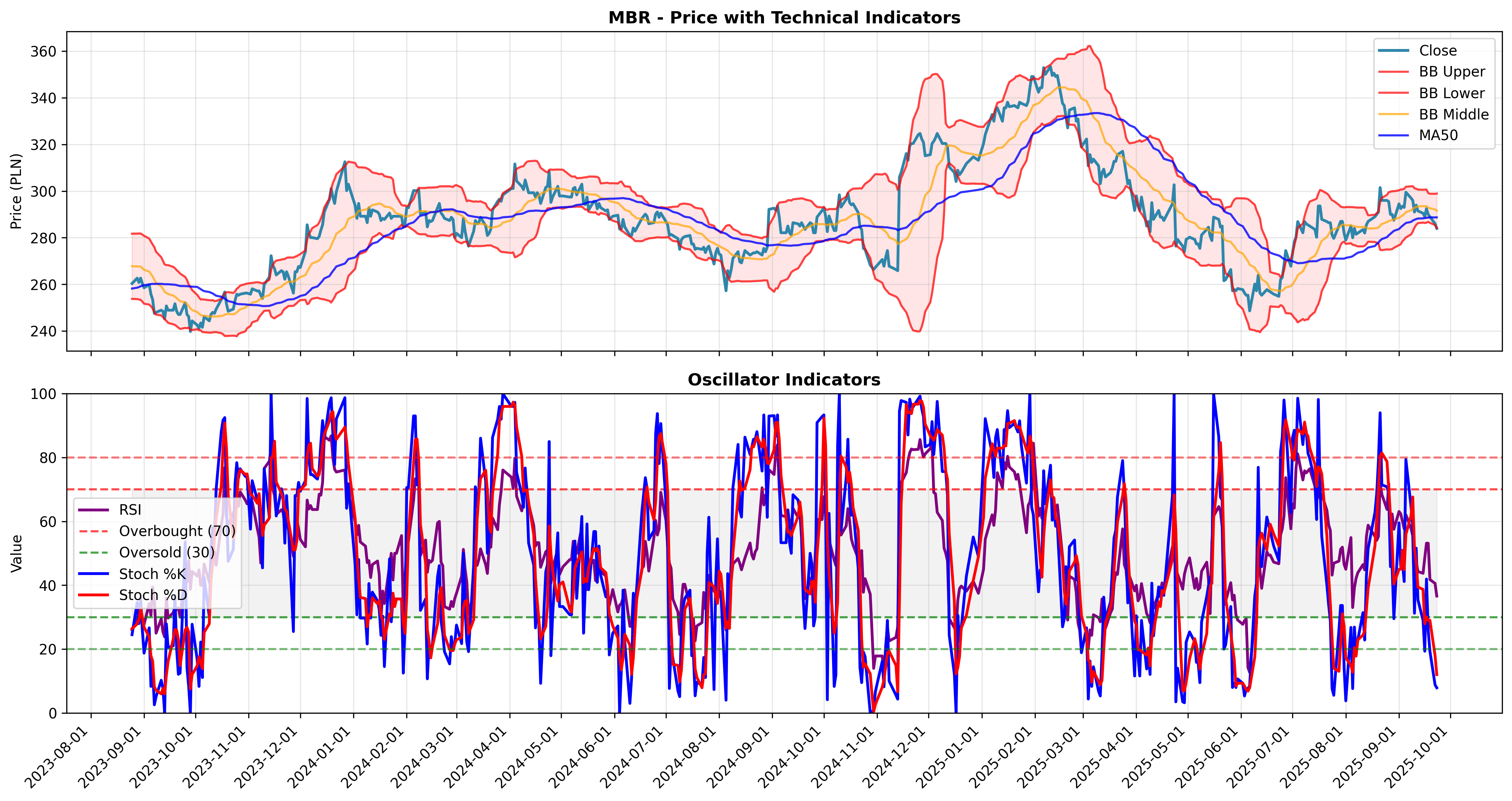

🔴 Bollinger Oscillators: Last SELL on 2025-08-21

- 📊 Total Confidence: 0.0%

- 🟢 Composite: 0.0%

- 🔵 Conservative: 0.0%

- 🔴 Aggressive: 0.0%

- 🟡 Institutional: 0.0%

- 🟣 Quantitative: 0.0%

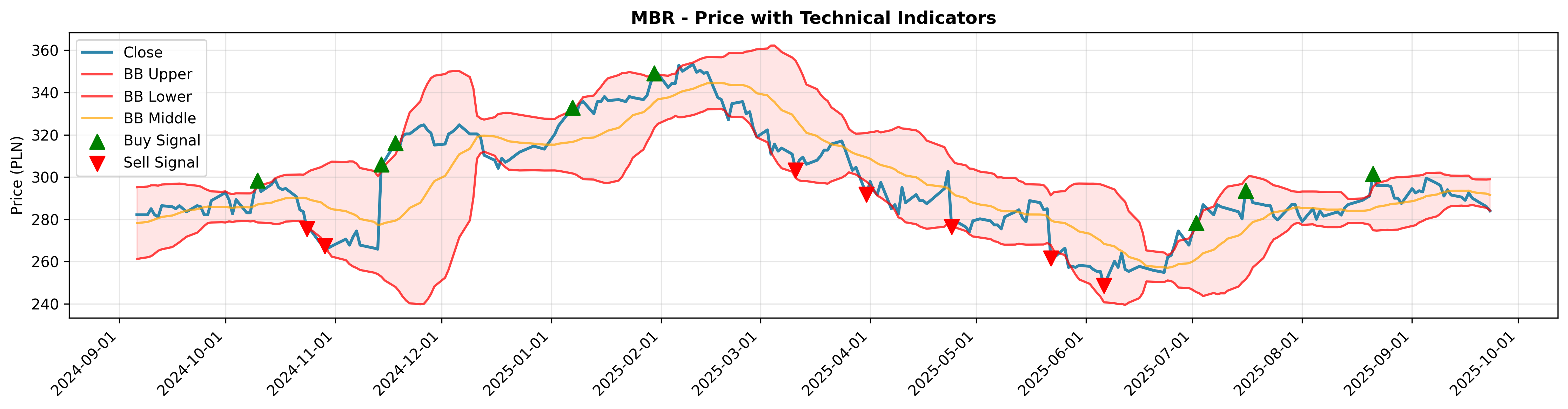

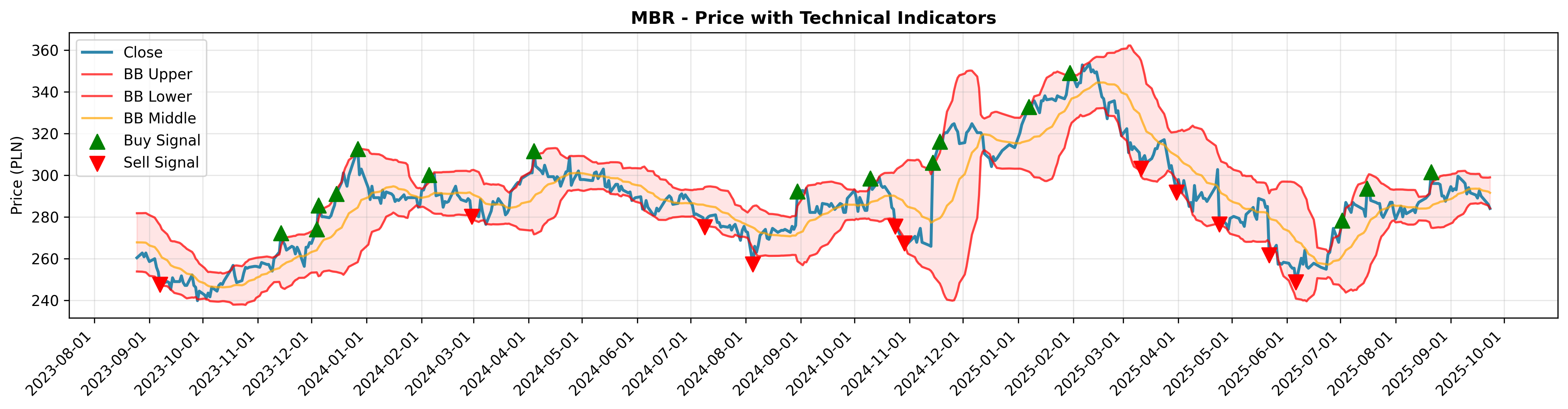

🟢 Breakout Momentum: Last BUY on 2025-08-21

- 📊 Total Confidence: 18.0%

- 🟢 Composite: 22.6%

- 🔵 Conservative: 0.0%

- 🔴 Aggressive: 18.9%

- 🟡 Institutional: 23.2%

- 🟣 Quantitative: 25.5%

🟢 Relative Strength Rotation: Last BUY on 2025-07-11

- 📊 Total Confidence: 25.2%

- 🟢 Composite: 30.6%

- 🔵 Conservative: 0.0%

- 🔴 Aggressive: 26.3%

- 🟡 Institutional: 32.6%

- 🟣 Quantitative: 36.7%

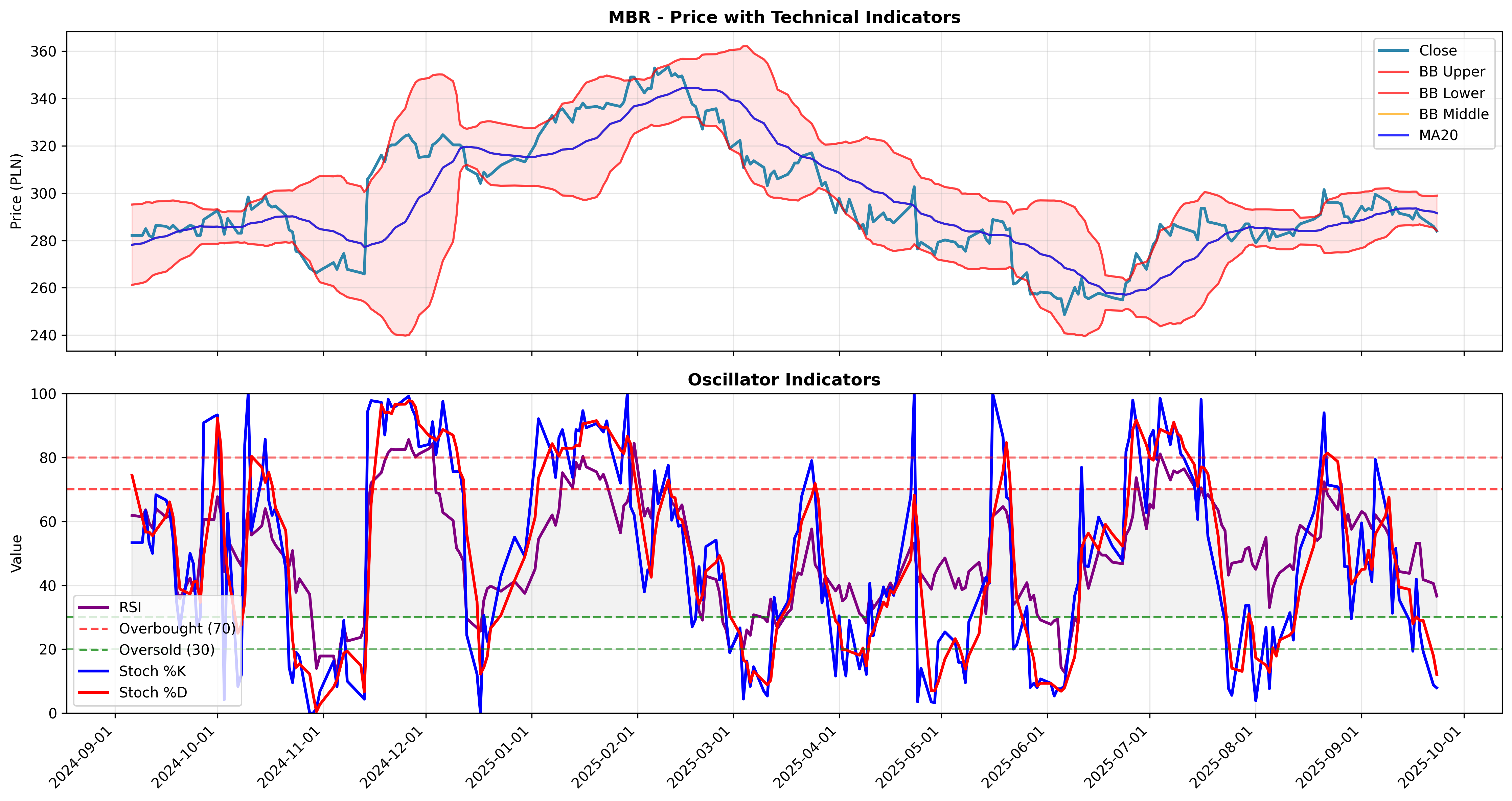

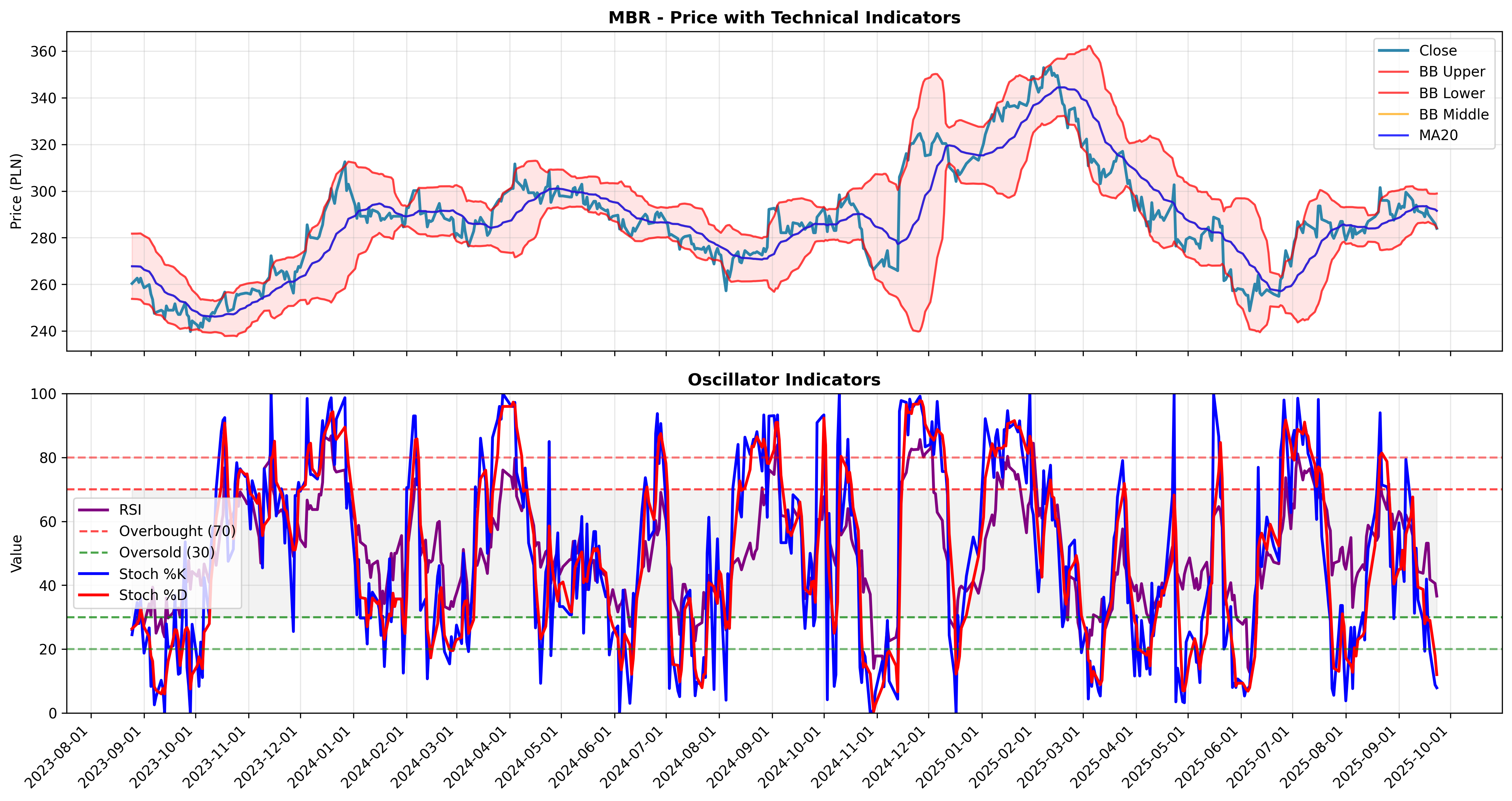

🟢 Gap Trading: Last BUY on 2021-11-22

- 📊 Total Confidence: 31.4%

- 🟢 Composite: 14.4%

- 🔵 Conservative: 21.6%

- 🔴 Aggressive: 17.3%

- 🟡 Institutional: 53.7%

- 🟣 Quantitative: 50.2%

🔴 Volatility Expansion: Last SELL on 2023-04-06

- 📊 Total Confidence: 24.9%

- 🟢 Composite: 33.7%

- 🔵 Conservative: 0.0%

- 🔴 Aggressive: 29.6%

- 🟡 Institutional: 35.0%

- 🟣 Quantitative: 26.1%

🔴 Momentum Kirkpatrick: Last SELL on 2025-09-23

- 📊 Total Confidence: 22.5%

- 🟢 Composite: 23.1%

- 🔵 Conservative: 0.0%

- 🔴 Aggressive: 19.2%

- 🟡 Institutional: 33.8%

- 🟣 Quantitative: 36.1%

📊 How Confidence Is Calculated

Confidence percentages tell you how much to trust a trading signal based on the strategy’s historical performance.

🎯 Current Method: Composite (Balanced)

- Sharpe Ratio: Up to 20 points (risk-adjusted returns)

- Win Rate: Up to 30 points (percentage of profitable trades)

- Total Return: Up to 50 points (overall profitability)

📈 Available Confidence Methods:

- 🟢 Composite (Balanced): Current method - balanced approach for most traders

- 🔵 Conservative (Risk-Averse): Emphasizes safety and downside protection

- 🔴 Aggressive (Growth-Focused): Prioritizes high returns over risk

- 🟡 Institutional (Modern Portfolio Theory): Professional fund management approach

- 🟣 Quantitative (Statistical): Mathematical and statistical measures

🎯 Confidence Levels:

- 70%+: Strong performer - trust this signal more

- 50-70%: Decent performer - moderate trust

- 30-50%: Weak performer - be cautious

- <30%: Poor performer - low trust

💡 Signal Interpretation

- 🟢 BUY signals: Suggest potential upward price movement

- 🔴 SELL signals: Suggest potential downward price movement

- ⚪ HOLD signals: Suggest maintaining current position

- 📊 Confidence: Higher percentages indicate stronger signal conviction

- 🎯 CONSENSUS: Overall recommendation based on multiple strategy agreement

📚 Detailed Confidence Method Explanations

🟢 Composite (Balanced) - Current Method

Formula: (Sharpe×20) + (WinRate×30) + (Return×50)

Used by: Individual traders, retail investors

Why: Balanced approach that considers risk, consistency, and returns equally. Good for most trading styles.

Example: Strategy with 0.4 Sharpe, 60% win rate, 80% return = (0.4×20) + (0.6×30) + (0.8×50) = 66% confidence

🔵 Conservative (Risk-Averse)

Formula: (Sharpe×25) + (WinRate×35) + (Return×40) - DrawdownPenalty + SafetyBonus

Used by: Pension funds, insurance companies, risk-averse investors

Why: Prioritizes capital preservation over growth. Heavily penalizes strategies with large drawdowns.

Key Features:

- Higher weight on consistency (win rate)

- Penalty for drawdowns >5%

- Bonus for low-risk strategies

- Caps returns at 50% to avoid overvaluing risky strategies

🔴 Aggressive (Growth-Focused)

Formula: (Return×60) + (Sharpe×15) + (WinRate×25) + HighReturnBonus

Used by: Hedge funds, growth investors, aggressive traders

Why: Maximizes returns regardless of risk. Suitable for investors who can tolerate volatility.

Key Features:

- 60% weight on raw returns

- Lower weight on risk adjustment

- Bonus for strategies with >50% returns

- Allows returns up to 200% contribution

🟡 Institutional (Modern Portfolio Theory)

Formula: InfoRatio + Consistency + RiskAdjustedReturn + ReturnComponent + SignificanceBonus

Used by: Mutual funds, pension funds, institutional investors

Why: Based on academic finance theory and institutional requirements. Emphasizes statistical significance.

Key Features:

- Information ratio (like Sharpe but more robust)

- Return-to-drawdown ratio

- Bonus for statistically significant results (>100 trades)

- Follows modern portfolio theory principles

🟣 Quantitative (Statistical)

Formula: CalmarRatio + SterlingRatio + WinRate + Return + SampleSize + StatisticalSignificance

Used by: Quantitative funds, algorithmic trading systems, research institutions

Why: Uses advanced statistical measures and mathematical optimization. Most rigorous approach.

Key Features:

- Calmar ratio (return/max drawdown)

- Sterling ratio (similar to Calmar)

- Sample size adjustment for statistical validity

- T-statistic proxy for significance testing

- Mathematical optimization of weights

🏛️ Financial Industry Context

Goldman Sachs: Uses similar multi-factor scoring for strategy selection

Renaissance Technologies: Employs statistical significance testing like our Quantitative method

Bridgewater: Emphasizes risk parity similar to our Conservative approach

AQR: Uses academic factors like our Institutional method

Two Sigma: Applies quantitative methods similar to our Statistical approach